How to Pay Yourself First (Without Destroying Your Budget)

Paying yourself first means saving money before you spend it on anything else. Set aside 10-20% of your income automatically before paying your necessities or buying anything.

What Pay Yourself First Actually Means (Most People Get This Wrong)

Most people think paying yourself first means stashing away whatever's left at the end of the month. That's backwards thinking that keeps you broke. This is what it really means:

It's not about saving leftover money

Save 10-20% of your paycheck before you pay any bills or buy anything else. This is in contrast to the traditional savings approach, which involves saving whatever's left over, which is usually nothing.

Your savings become a non-negotiable expense, like rent or your phone bill. You wouldn't skip paying rent because you wanted to buy something, so treat your savings the same way. Whatever money is left over after saving is what you have available for everything else.

It's about flipping the script on how money flows

This approach removes the decision-making from saving because the money disappears before you can spend it. Here's what changes:

- Money is automatically saved before it can be categorised as "spendable," eliminating the mental battle of deciding whether to save or spend.

- You're forced to live on less, which naturally makes you more conscious about spending without needing constant willpower or complicated budgeting systems.

- Spending impulses and lifestyle inflation can't touch your savings because the money isn't available.

Your savings grow consistently because they're protected from your spending impulses, lifestyle inflation, and those "just this once" purchases that happen every month. The system works because it fights against human psychology instead of relying on it.

It's not just one big savings account

When paying yourself first, you're not just dumping it into one savings account. You should be breaking down your savings into these categories:

- Emergency fund: 3-6 months of expenses in a high-yield savings account for unexpected costs like car repairs, medical bills, or job loss.

- Retirement savings: Money going into 401k, IRA, or other retirement accounts you can't touch for decades.

- Wealth building: Investment accounts for long-term goals like buying a house, starting a business, or achieving financial independence.

These accounts give you options and opportunities most people never have. To make it a little easier, consider opening a savings account with buckets (or envelopes) that make it easier to differentiate your savings.

How to Pay Yourself First Without Destroying Your Life

Paying yourself first works, but only if you implement it correctly. Jumping in too aggressively will create financial stress that will force you to abandon the system entirely.

Start with the right percentage for your situation

Aim for 20% of your gross income if possible, but start with whatever you can consistently do without creating financial stress. Here's how to approach it:

- Start with 5% or even 1% if 20% feels impossible, because building the habit matters more than the amount initially.

- Build the habit first because you can always increase the amount later, but you can't build consistency without starting somewhere manageable.

- Increase your savings rate by 1% every six months until you reach your target, which gives you time to adjust your spending gradually.

Don't compare your savings rate to others. A person making $40,000 saving 10% is doing better than someone making $100,000 saving 5%. Your situation is unique, and consistency beats perfection every time.

Set up automatic transfers that happen before you can touch the money

Schedule automatic transfers for the day after your paycheck hits your account, when your balance is highest, you're less likely to notice the money leaving. Use direct deposit to send cash to savings before reaching your checking account.

Set up multiple automatic transfers to different goals: emergency fund, retirement, vacation fund. Each goal gets its automatic contribution, so you're making progress on everything simultaneously without having to remember or decide each month.

Choose the right accounts for different timeframes

Different savings goals need different account types. Match your timeframe to the right account:

- Emergency fund: High-yield savings account that's accessible but not connected to your everyday checking account (3-6 months of expenses).

- Retirement savings: 401k up to company match first, then Roth IRA, then back to 401k if you max the IRA.

- Medium-term goals: Separate high-yield savings accounts for each goal, like house down payments or vacation funds.

- Long-term wealth building: Taxable investment accounts with low-cost index funds for opportunities and financial independence.

Don't mix your vacation fund with your car replacement fund. Keep each goal separate so you can track progress and avoid accidentally spending vacation money on car repairs. For more tips on money management, you can read my article, How to Manage Your Money (10 simple steps to gain control of your finances).

Why Most People Never Save Money (And You're Probably One of Them)

Even people who understand they should save money still struggle to do it. The problem isn't a lack of knowledge or motivation; most people use a system designed to fail.

You pay everyone else first, then save the scraps

The traditional money flow keeps you broke because it follows this broken sequence:

- You pay all your bills first, including rent, utilities, insurance, and those subscriptions you forgot you even had.

- You spend on whatever catches your eye throughout the month, like dining out, shopping, and entertainment, which seems reasonable.

- You save whatever's left over, usually nothing, because spending always expands to fill available money.

- You promise you'll do better next month when things "calm down," but next month never comes.

You tell yourself you'll save next month when things calm down. Next month never comes because there's always another expense, emergency, or thing you "need" to buy. This backward approach means your future self always loses to your present self's spending desires.

Every month, you promise to do better, but the system works against you. Without changing the order of operations, you're fighting a losing battle against human nature.

You're fighting human psychology and losing

Spending expands to fill whatever money is available in your checking account. Give yourself $3,000 to spend and you'll find ways to spend exactly $3,000 on things that suddenly seem important.

Your brain treats money in checking accounts as available to spend, even if you intellectually planned to save it. Without a system, saving becomes a willpower battle you'll lose every time you're tired, stressed, or see something you want to buy.

The solution isn't more willpower or better intentions. It's a system that removes the decision entirely by moving money before your brain can categorize it as spendable. This is why my Conscious Spending Plan works so well alongside paying yourself first; it creates structure that works with your psychology, not against it.

The Real Cost of Not Paying Yourself First

The numbers are staggering when you see what delaying actually costs you.

Missing out on compound growth over decades

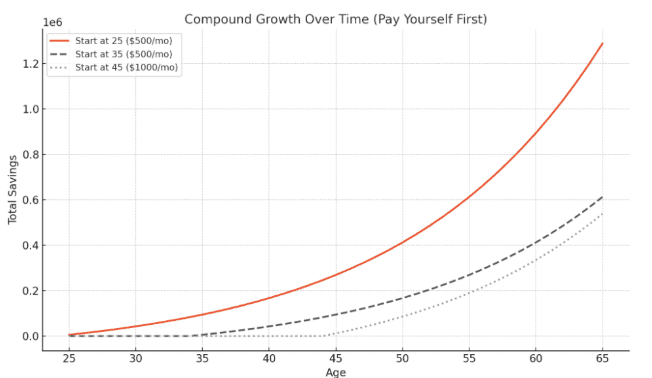

When it comes to investing, starting early beats saving more later because compound interest does the heavy lifting for you. Someone who saves $500 monthly starting at age 25 will have over $1.3 million by retirement. Wait until age 35 and you'll have half that amount, even though you only delayed 10 years.

That's the power and the penalty of compounding. But it doesn't stop there.

For example, if you start at 45 instead of 35, and even if you double your monthly savings to $1,000, you'll still end up with far less than the person who started earlier with half the effort. Compound interest doesn't reward those who show up late. It rewards those who show up early.

A 25-year-old saving $300 a month will end up with more than a 35-year-old saving $600. Likewise, a 35-year-old saving $600 will likely outpace a 45-year-old saving $1,000. Each decade you delay costs you more and gives you less in return.

The longer you wait, the more expensive and difficult it becomes to catch up.

Living paycheck to paycheck forever

Living paycheck to paycheck takes a toll on you. Without savings, every emergency becomes a crisis that requires debt to solve. Your car breaks down, and suddenly you're paying 20% interest on a credit card for something that should have been handled with cash.

Car repairs, medical bills, and job losses can become high-interest credit card debt that takes years to pay off. You may end up paying thousands more for the same emergency because you didn't have cash ready.

You become trapped in a cycle where you can't take risks or opportunities because you have no financial cushion. This keeps you stuck in jobs you hate and situations you want to escape.

Missing life opportunities that require money

Just like how emergencies can throw you off budget, life can also bring you unexpected opportunities, which may require an initial investment upfront. Without savings, you miss out on:

- Business opportunities slip away while you're scrambling to figure out financing, and someone else with cash ready takes your spot.

- Market crashes become missed chances to buy quality investments when they're cheap, because you don't have the money to invest.

- Career transitions become impossible because you can't afford to take time off to find better opportunities or retrain for new skills.

- Educational opportunities that could boost your earning potential get skipped because you can't afford tuition or time away from work.

You stay in a job you hate because you can't afford to take time off to find something better. Financial stress forces you into career decisions based on desperation rather than opportunity.

Damage to relationships and family finances

Without savings, money stress seeps into every relationship and major life decision. Dawn and Richard, a couple from my podcast, show how the lack of a pay yourself first system can destroy even the strongest relationships.

They're living paycheck to paycheck despite making six figures combined. Although they're engaged, they're struggling to combine their finances because Dawn overspends on her kids and grandkids while Richard has deep scars from a financially devastating breakup. Here's what happened when they tried to save money the traditional way:

| [00:10:05] Ramit: Why are we here?

[00:10:06] Dawn: Because I guess I thought we would have extra money that we could– because that was our plan. Like, oh, we’ll each put like 50 into a savings for this, and we’ll have an emergency fund. But then I realized when he gives me the 200, it still just pays the bills. There’s still not a lot of extra. We’re just not doing any saving or anything. We have no emergency fund. We have nothing. [00:10:30] Ramit: Is this a problem for you, Richard? [00:10:32] Richard: It is. At the end of the day, we just want structure. I have the ability to put money aside, but it’s, now where do I put it? |

This is what happens when you rely on leftover money to save. Dawn and Richard had good intentions and even made a plan, but without paying themselves first, their savings goals got consumed by bills and daily expenses. Their relationship stress grew because they both wanted financial security, but couldn't figure out how to make it happen with their current approach.

When Pay Yourself First Doesn't Work

Putting yourself first is powerful, but it's not the right move for everyone in every financial situation. Sometimes you need to handle other priorities before implementing this strategy.

You have high-interest debt

If you're paying 20%+ interest on credit cards, focus on killing that debt first before building wealth. No investment will reliably beat 20% returns, so paying off credit cards IS your best investment.

There's one important exception to this rule. You should save a small emergency fund of $1,000-2,000 to avoid creating more debt when emergencies happen. Without this buffer, car repairs and medical bills force you deeper into debt.

Once high-interest debt is gone, redirect those monthly payments to paying yourself first. If you were paying $400 monthly toward credit cards, that same $400 can now build wealth instead of paying interest.

Your income barely covers basic necessities

If you're living paycheck to paycheck on necessities (not lifestyle choices), focus on increasing income before optimizing savings rates. Your time is better spent developing skills or finding higher-paying work.

Even saving $25 monthly builds the habit and creates momentum for when your income increases. The muscle memory of automatic saving will serve you well when you have more money.

You haven't built the foundation yet

You must get your 401(k) company match before anything else. This is free money that doubles your contribution instantly. Skipping the match is like leaving money on the table.

You should also build a small emergency fund of $1,000-2,000 before focusing on long-term wealth building. Without this, every unexpected expense derails your financial progress and forces you into debt.

If you want to see the complete foundation for building wealth, including these basics and beyond, check out my breakdown of the 10 money rules that create life-changing wealth:

Your Rich Life + Pay Yourself First System

Once you understand the concept and timing, you need a system that works in real life. The goal is to build wealth automatically while still enjoying your money today.

Automate everything so money decisions happen without you

Your system should run itself once you set it up. Configure automatic transfers, then check quarterly to make adjustments based on income changes or new goals.

Use the money left over for bills and spending after you've paid yourself first. This will remove guilt from spending because you've already secured your future.

Increase savings automatically when you get raises, so lifestyle inflation doesn't eat your extra income. For example, if you get a $200 monthly raise, automatically send $100 to savings before you get used to spending it.

Make your automated savings work toward your Rich Life

Don't just save for the sake of saving or because someone told you to. Connect each dollar to specific goals that excite you and align with your vision of a Rich Life.

Your emergency fund buys you freedom from financial stress and bad situations. It's insurance against life's surprises and the foundation that lets you take smart risks.

Retirement savings give you the choice to work because you want to, not because you have to. Investment accounts give you options and opportunities that most people miss. Whether you're starting a business, buying real estate, or taking advantage of market opportunities, having money ready creates possibilities.

Focus on the big wins instead of micromanaging every dollar

Getting your savings rate right matters 100x more than optimizing which high-yield savings account pays 0.1% more interest. This is precisely what focusing on the Big Wins is all about. Instead of getting lost in tiny details, concentrate your energy on the moves that change your financial life:

- Increase the amount you save rather than optimizing tiny account differences that might earn you a few dollars annually.

- Earn more money rather than cutting your coffee budget or tracking every expense in budgeting apps that stress you out.

- Set up automation once instead of constantly managing transfers and second-guessing your system every month.

- Maximize employer 401(k) matches before worrying about investment fees that make a minimal difference to your returns.

The beauty of this system is its simplicity. Instead of tracking every expense in budgeting apps, pay yourself first, then spend the rest guilt-free on things you love. Once you've secured your future, you can enjoy your present without financial anxiety.

Stay in the know

Be the first one to receive new releases,

special offers, and more