Market Timing: Why It Doesn’t Work (And What To Do Instead)

Market timing is basically people yanking money in and out of investments out of fear or greed. While it sounds incredibly appealing to buy low and sell high with perfect precision, nobody can consistently predict what the market will do next. Honestly, most investors who try to “time the market” get the exact opposite of what they wanted.

What People Really Mean When They Say "Market Timing"

Market timing doesn't work for most people, period. The concept sounds brilliant until you actually try to do it.

The typical market timer waits for the "perfect moment" to invest. They sit on cash, watching the market climb, waiting for a dip that might never come. Then, when a crash finally happens, they panic and sell at the worst possible moment instead of buying. Later, after the market recovers and hits new highs, they finally buy back in at inflated prices.

This is the opposite of buying low and selling high. But it's what happens to most people who try timing the market.

Why Market Timing Turns Smart People Into Financial Disasters

Here's what typically happens when people attempt to time the market:

Market timing creates an illusion of control you don't actually have

Market timing appeals to people because it creates an illusion of control. You feel like you're actively managing your money instead of just letting it sit there. You're making moves, analyzing trends, outsmarting the masses.

This feeling is seductive. It makes you feel smart and engaged with your finances. But feeling smart and actually building wealth are two completely different things.

The market doesn't care about your analysis or gut feelings. It moves based on millions of factors you can't possibly track or predict. Trying to outsmart it usually just means tripping over your own strategy.

Professional investors can't time the market either

If market timing worked, professional fund managers would consistently beat the market. They have teams of analysts, real-time data, sophisticated algorithms, and decades of experience. They do this full-time as their career.

Yet studies show that over 80% of actively managed funds underperform simple index funds over 10-year periods. These are the experts, and they can't consistently time the market either. What makes you think you can do better from your laptop while working a full-time job?

The answer is you can't. Nobody can. And pretending otherwise just costs you money.

You'll miss the best days (and they happen when you least expect them)

The strongest rallies usually occur right after the market’s ugliest drops. This counterintuitive timing is exactly why market timing fails so spectacularly.

When the market crashes and fear dominates the news, that’s precisely when you should stay invested. But it’s also exactly when market timers sell in panic. Then the market rebounds before they get back in, causing them to miss the recovery entirely.

The cost of missing these rebounds is staggering. Consider what happened between 2000 and 2020, a period that included the dot-com crash, the 2008 financial crisis, and the 2020 pandemic crash. If you invested $10,000 in the S&P 500 at the start of 2000 and simply stayed invested through all the chaos, you’d have around $32,000 by 2020.

But here’s where the numbers get brutal. The market’s “best days” are the single trading days when stocks jumped the most. These are the days when the S&P 500 gained 5%, 7%, or even 10% in a single session. Missing just a handful of these massive up days would dramatically tank your returns.

For example, missing just 10 best days out of more than 5,000 trading days cuts your returns in half, dropping your portfolio from $32,000 down to about $16,000. Miss 20 of the best days and you’re left with less than $12,000. Miss 30 best days and you’d actually lose money, ending up with only $8,000.

Those 10 days that make or break your returns are impossible to predict in advance. They typically happen right in the middle of market crashes when everything feels hopeless and selling seems like the smart move.

Those best days cluster around the worst crashes

Here's what makes this even more cruel. Those best single-day gains often happen in the immediate aftermath of terrible crashes. In March 2020, when COVID-19 panic was everywhere and the market was collapsing, some of the biggest single-day gains in history occurred just weeks after the largest losses.

If you sold during the initial panic and waited for things to "stabilize," you missed those massive bounce-back days. By the time you felt comfortable reinvesting, the market had already recovered most of its losses.

The same pattern happened in 2008-2009. The market's best days came while everything still felt terrible. People who sold and waited for a "safe" entry point missed the entire early recovery.

The "perfect" entry point is a myth that costs you real money

Chasing the perfect entry point is a money drain. Nobody, not even professionals with unlimited resources, can consistently identify market bottoms before they happen.

You might get lucky once. Maybe twice. But you'd need to be right about 75% of the time just to keep up with a simple buy-and-hold strategy in an index fund. Research has proven this repeatedly. Almost nobody clears that bar, especially not over multiple years.

Meanwhile, all that hesitation and second-guessing burns time. Time is the one thing that actually builds wealth through compound growth. Every month you sit on cash waiting for the perfect moment is a month of potential gains you'll never get back.

Your emotions will sabotage you every single time

Fear and greed are terrible investment advisors, but they're what actually drive market timing decisions. This isn't a character flaw. It's human nature, hardwired into your brain.

When the market crashes and you're watching your account balance drop by thousands of dollars every day, fear screams at you to sell before you lose everything. The news amplifies this with doom-and-gloom headlines about how bad things might get.

When the market is soaring and everyone around you is making money, greed tells you to buy more. You don't want to miss out. You see others getting rich and feel left behind.

Here's what emotional decision-making does to your returns:

- Fear makes you sell during crashes at the absolute worst time, locking in losses permanently.

- Greed makes you buy during peaks right before corrections, maximizing your losses.

- Regret paralyzes you after mistakes, causing you to miss recovery opportunities.

- Overconfidence after lucky wins encourages increasingly risky bets that eventually fail.

This emotional rollercoaster is why most market timers end up buying high and selling low. It's the exact opposite of what they intended, but it happens to almost everyone who tries to time the market based on feelings rather than discipline.

The data doesn't lie about investor behavior

Studies tracking actual investor behavior show this pattern clearly. During market downturns, money floods out of stock funds as people panic-sell. During bull markets, money floods back in as people chase returns.

One study from Quantitative Analysis of Investor Behavior (QAIB) found that the average investor earned only about 4% annually over 20 years when the S&P 500 returned about 8% annually. The difference was entirely due to poor timing decisions, such as buying high and selling low based on emotions.

You're not immune to this. Nobody is. Knowing about these biases doesn't make you immune to them. The only way to avoid emotional timing mistakes is to not try timing the market at all.

Transaction costs and taxes eat your profits alive

Every time you jump in and out of the market, you're paying transaction fees and potentially triggering taxes. These costs might seem small individually, but they compound into serious money over time.

If you hold investments for less than a year before selling, you'll pay short-term capital gains taxes. These can be as high as your regular income tax rate, potentially 37% at the federal level for high earners, plus state taxes on top.

Compare that to long-term capital gains rates of 0%, 15%, or 20% if you hold for more than a year. The difference between 37% and 15% tax rates on a $10,000 gain is $2,200. That's real money you're giving to the government just because you couldn't wait 12 months.

The math gets worse with frequent trading

Let's say you're an active market timer making trades throughout the year. You buy and sell 10 times, each time triggering a taxable event. If each trade generates a $1,000 gain and you're paying 30% in short-term capital gains tax, you're giving up $3,000 total.

Meanwhile, someone who bought and held paid zero taxes during that year. Their money keeps compounding tax-free until they eventually sell years later at the lower long-term rate.

This doesn't even count trading commissions or fund expense ratios. Active traders often use actively managed funds with expense ratios of 1% or higher. Index funds charge 0.03% to 0.20%. That difference compounds dramatically over decades.

What To Do Instead of Chasing “Perfect” Timing

Now that you know why timing the market is a losing game, here's what actually works. These strategies are boring, and that's precisely why they succeed.

Invest in boring, low-cost index funds

Forget trying to pick individual stocks or time the market. Put your money in broad market index funds with low fees and let compound growth do the work.

The S&P 500 has delivered an average annual return of about 10% over the past 20 years, despite multiple crashes, recessions, and global panics. That includes the dot-com bust, the 2008 financial crisis, the 2020 pandemic crash, and everything in between.

This approach takes no special skill, barely any effort, and still outperforms most professional fund managers over time. You don't need to be smart or lucky. You just need to be consistent and patient.

If you want concrete recommendations, here are the funds to start with:

- Vanguard Total Stock Market Index Fund (VTSAX or VTI) gives you exposure to the entire U.S. equity market in one investment.

- Vanguard Total International Stock Index Fund (VTIAX or VXUS) covers international markets for global diversification.

- Vanguard Total Bond Market Index Fund (VBTLX or BND) covers the entire U.S. bond market and adds stability to your portfolio.

- All three Vanguard funds charge tiny fees of 0.05% to 0.15% annually, compared to 1% or more for actively managed funds.

These funds aren't fancy or exciting. You're getting the entire market at minimal cost, which is exactly what works for building long-term wealth without the stress of timing decisions.

Rebalance periodically, not emotionally

Rebalancing means adjusting your portfolio back to your target allocation. If you decided on 70% stocks and 30% bonds, but stocks have grown to 80% of your portfolio, you'd sell some stocks and buy bonds to get back to 70/30.

This is not market timing. You're not trying to predict which direction the market will go. You're maintaining a consistent risk level by selling things that have gone up and buying things that have gone down.

Do this once or twice a year on a fixed schedule. Don't do it based on how you feel about the market or what the news is saying. Calendar-based rebalancing removes emotion from the equation entirely.

Set up automatic investments and never think about timing

The best way to avoid market timing is to automate your investments completely. Set up automatic transfers from your paycheck or checking account into your investment accounts on a fixed schedule.

This is called dollar-cost averaging, though you don't need to know the fancy term. You're simply investing the same amount regularly regardless of what the market is doing. Sometimes you'll buy when prices are high, sometimes when they're low. Over time, this averages out to reasonable prices without requiring any timing decisions from you.

If you invest $500 every month for 30 years at an average 8% return, you'll have over $680,000. That's with zero market timing, zero stock picking, and zero stress about whether you're buying at the "right" time.

If you absolutely must scratch the timing itch, use play money

Look, I get it. Sometimes you want to feel like you're doing something active with your investments. The urge to time the market or pick individual stocks can be overwhelming.

If you absolutely can't resist high-risk investments or timing fun, limit it to 5-10% of your portfolio. This is money you can afford to lose completely without impacting your financial future.

Think of this as your "play money" for speculation. Put 90-95% of your investment money in boring index funds following the strategies above. Use that small 5-10% to scratch your market timing itch, pick individual stocks, or make speculative bets.

What usually happens with play money

When you lose that play money (not if, when), you'll still be building wealth with the majority of your portfolio. The 90% in index funds will keep growing steadily while you learn expensive lessons with your 5%.

Most people who do this find that their play money account significantly underperforms their boring index fund account. This firsthand experience is often what finally convinces them to stop trying to time the market.

That's actually valuable. Think of it as paying tuition to learn why market timing doesn't work. As long as you keep the amount small, it's a relatively cheap education that might save you from making much bigger mistakes later.

Focus on time in the market, not timing the market

The single most important factor in building wealth through investing is how long you stay invested. Time in the market beats timing the market every single time.

Someone who invested $10,000 at the worst possible moment in 2007, right before the financial crisis, would still have over $40,000 today if they held through all the ups and downs. Someone who tried to time their way around the crisis probably has much less.

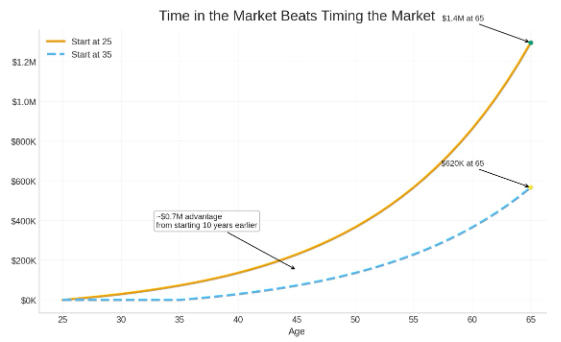

The earlier you start and the longer you stay invested, the more compound growth works in your favor. A 25-year-old investing $5,000 annually will have about $1.4 million by age 65, assuming 8% returns. A 35-year-old investing the exact amount will only have about $620,000.

That 10-year difference in starting time is worth over $750,000. No amount of market timing skill will make up for starting late or pulling money out during downturns. Here’s what that difference looks like when you start investing early. You can see how time in the market compounds far faster than trying to time it.

Stop Timing and Start Living Your Rich Life

Market timing might sound exciting, but it's a distraction from what really counts: building steady wealth you can actually use. The goal isn't to beat the market or feel smart about your investment decisions.

The goal is to grow your money so you can spend on what you care about without guilt. Here's what focusing on your Rich Life instead of market timing looks like:

- Index funds compound quietly in the background while you focus on your career, relationships, and hobbies.

- You avoid the stress of watching financial news and worrying whether this is the "right" time to invest.

- Your mental energy goes toward things that actually improve your life instead of obsessing over market movements.

- You build real wealth through consistency rather than gambling on perfect timing that never comes.

Set up automatic investments in low-cost funds and move on with your life. The people who build real wealth aren't the ones making dramatic market timing calls. They're the ones who invested consistently in boring funds for decades while everyone else was panicking or chasing returns. Be boring. Get rich. Live your Rich Life.

Stay in the know

Be the first one to receive new releases,

special offers, and more