FatFIRE Explained (Building Your Multimillion-Dollar Retirement)

FatFIRE is the luxury version of financial independence, requiring $2.5 to $10 million in investments to support annual spending of $ 100,000-$300,000+ in retirement. This approach provides ultimate retirement comfort but requires strategic high-income career paths, a high savings rate, and smart investment choices.

What Is FatFIRE And How Much Do You Need?

FatFIRE gives you the luxury version of financial freedom. Unlike other approaches that cut back on spending, FatFIRE lets you enjoy retirement without money worries.

People aiming for FatFIRE typically want at least $2.5 million to $5 million saved up. Many shoot for $5 to $10 million so they can maintain their lifestyle forever just from investment returns.

FatFIRE vs. Other FIRE Methods

FatFIRE is just one of many different retirement dreams that have gained popularity after the FIRE (Financial Independence, Retire Early) approach. Here’s a look at FarFIRE vs other FIRE methods:

Key differences in retirement spending levels

The FIRE movement has several variations, each with different spending levels and required investment amounts.

- FIRE: The standard Financial Independence, Retire Early approach typically aims for annual spending of $40,000 to $80,000, requiring roughly $1 million to $2 million in investments.

- FatFIRE: The luxury version supports annual spending of $ 100,000 to $300,000+, requiring investments of $2.5 million to $7.5 million or more to sustain it indefinitely.

- ChubbyFIRE: The middle ground between FIRE and FatFIRE, supporting annual spending of $80,000-$150,000, requiring approximately $2 million to $3.75 million in investments.

- LeanFIRE: The most frugal approach with annual spending under $40,000, requiring roughly $1 million or less in investments, often involving significant lifestyle downsizing.

These different FIRE approaches show that financial independence comes in many forms, and your personal values and lifestyle goals should determine which path makes the most sense for you.

Income requirements for FatFIRE

Let's examine the math behind FatFIRE to understand how much you need to save.

Using the 4% rule, you need to invest approximately 25 times your annual expenses to sustain your lifestyle indefinitely. The 4% rule suggests you can withdraw 4% of your investment portfolio in the first year of retirement, then adjust that amount for inflation each year after.

For an annual spending of $150,000, that means $3.75 million invested. This amount should last through your retirement years based on historical market performance.

Many FatFIRE pursuers use a more conservative 3-3.5% withdrawal rate for added security, which increases the required investment total to $4.3 million to $5 million for an annual spending of $150,000.

Lifestyle expectations with FatFIRE

Once you reach FatFIRE, your day-to-day life changes dramatically with new options and freedoms.

FatFIRE retirees enjoy premium experiences without money stress. This includes first-class travel, luxury hotels, fine dining, and lots of spending on things you enjoy.

Owning homes without mortgages in nice areas is common. Many also have vacation properties or second homes in top locations.

Healthcare options go beyond basic insurance to include personal doctors, specialists outside your network, and procedures not covered by standard insurance. All of these luxuries are exactly why FatFIRE is so enticing.

How Much Money Do You Need For FatFIRE?

Now that we understand what FatFIRE means, let's look at specific numbers to make this concept more concrete.

Common FatFIRE net worth targets

FatFIRE usually starts at $2.5 million, which supports around $100,000 in yearly spending using the 4% withdrawal rule. Many FatFIRE fans aim for $5 million, which allows for about $200,000 in yearly spending with a carefully calculated withdrawal rate.

High-end FatFIRE seekers want $10 million or more, allowing for yearly spending of $300,000 to $400,000 while keeping their money growing for future goals or increased spending.

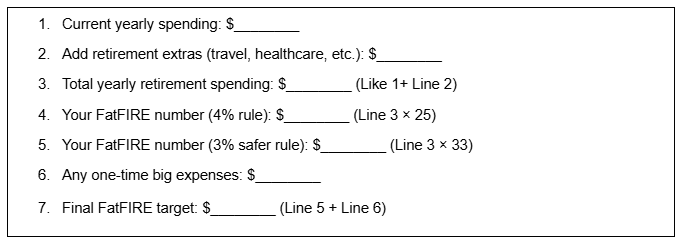

Calculate your personal FatFIRE number

Start by tracking what you spend now. Then add desired lifestyle upgrades and extra retirement costs, such as better healthcare, to determine your target yearly spending. Here’s some basic information you’d need to consider:

Here’s what the math looks like, all laid out for someone who spends $80,000 a year:

- If you currently spend $80,000 annually but want to travel more extensively in retirement (adding $30,000) and expect higher healthcare costs of $15,000, your target becomes $125,000.

- Multiply your target yearly expenses by 25 (using a 4% withdrawal rate) or 33 (using a more careful 3% rate) to calculate how much you need invested.

- $125,000 × 25 = $3.125 million, or $125,000 × 33 = $4.125 million for a more conservative approach.

- Add any significant one-time expenses you expect, such as paying for your children's college, buying a vacation home, or making large donations. If you plan to help two children with college ($200,000 each) and buy a vacation home ($500,000), you'd add $900,000 to your number.

Keep in mind that inflation will also affect your calculations. What costs $125,000 today might cost $180,000 in 20 years. So, adjust your targets periodically as you approach your Fat FIRE date. For more detailed calculations, check out my Retirement Calculator Tool.

Regional cost differences and their impact

Where you choose to live can dramatically affect how much money you need for a FatFIRE.

FatFIRE in expensive coastal cities like San Francisco or New York might require 50-100% more money than achieving the same lifestyle in cheaper areas like Charlotte or Nashville. The same $5 million that funds a lavish lifestyle in Phoenix might barely cover a comfortable upper-middle-class life in Manhattan.

Living abroad can dramatically reduce FatFIRE requirements. Luxury living in countries like Portugal, Mexico, or Thailand might cost 30-50% less than in the U.S. Some FatFIRE retirees go as far as to become "half-pats," spending part of the year in lower-cost countries to stretch their dollars further.

Property taxes vary significantly by location and can have a substantial impact on long-term FatFIRE success. They range from almost nothing in some states to tens of thousands of dollars per year in others. For example, a $1 million home might have annual property taxes of $1,000 in Hawaii versus $25,000 in parts of New Jersey.

Strategies To Achieve FatFIRE

With your target number in mind, let's explore the most effective ways to reach your FatFIRE goal.

High-income career paths

Traditional high-paying jobs, such as medicine, law, and finance, offer clear paths to FatFIRE, particularly for specialists earning $300,000 to $1 million or more per year. Neurosurgeons, corporate attorneys, and investment bankers often have the income potential to reach FatFIRE in 15-20 years.

Tech industry roles, especially in engineering management, product management, and specialized development, can speed up FatFIRE timelines through high salaries and stock options. Senior software engineers at top companies now regularly earn over $300,000, with total compensation packages.

Executive advancement remains a powerful FatFIRE enabler. C-suite positions offer pay packages that can compress the journey to 10-15 years of focused saving and investing. A Chief Financial Officer at a mid-sized company might earn $400,000-$700,000 annually, creating a clear path to FatFIRE.

Entrepreneurship and business ownership

Building and selling a business is often the fastest path to financial freedom (FIRE) for many. Successful exits often yield multi-million-dollar payouts that instantly create FatFIRE-level wealth. Even modest businesses selling for 3-5 times annual profit can generate significant wealth when built intentionally.

Online businesses with low overhead and high growth potential have created a new wave of FatFIRE achievers. Platforms, software products, and digital content can have profit margins of 70-90%. Software-as-a-service (SaaS) businesses, in particular, can sell for 5 to 15 times their annual recurring revenue.

Buying and growing existing businesses offers a middle path with lower risk than starting a new business, but higher returns than traditional jobs. This works exceptionally well with seller financing and proven business models.

The truth is, almost anyone can become a successful entrepreneur with the right direction. If you don’t know where to start, check out my articles:

- Entrepreneurial Mindset: What Is It and How to Think Like One

- How to Become an Entrepreneur in 6 Steps

Smart investment strategies over a long period of time

Consistent investing in broad market index funds remains the foundation for most FatFIRE portfolios. Compound growth does the heavy lifting over 15-25-year savings periods. Consider these key investment strategies for FatFIRE:

- Maximize tax-advantaged accounts first. Contribute the maximum allowed to 401(k)s, IRAs, HSAs, and other tax-advantaged vehicles before investing in taxable accounts.

- Automate your investments. Set up automatic transfers on payday to ensure you consistently invest before you have a chance to spend.

- Use dollar-cost averaging. Invest regularly, regardless of market conditions, to reduce the impact of market volatility and avoid making emotional decisions.

Tax planning through strategic use of retirement accounts, tax-loss harvesting, and capital gains management can add 1-2% yearly to your returns. This dramatically impacts your final portfolio size. Over 30 years, an extra 1% annual return can increase your final portfolio by more than 30%.

Eliminate all debt as soon as possible

Getting rid of high-interest consumer debt is a non-negotiable step. Credit card and personal loan interest rates make wealth building mathematically impossible. Credit cards charging 18-25% interest will always outpace even excellent investment returns.

Student loan management requires strategic thinking. Depending on loan terms and career path, forgiveness programs, refinancing, and accelerated payment options all have potential benefits.

A doctor with $300,000 in student loans might be better off pursuing Public Service Loan Forgiveness, while a tech worker might focus on refinancing to a lower rate and paying off the debt quickly.

Mortgage debt presents more nuanced choices. With mortgage rates around 4-5% and long-term stock market returns averaging 7-10%, the math often favors investing over paying off an aggressive mortgage.

If you need some help getting out of debt before starting your journey to FatFIRE, you can start with these articles:

- How to Get Out of Debt Fast (7 practical steps you can start now)

- Debt Avalanche vs Debt Snowball (which method is best for you)

Real estate investing for FatFIRE

Rental property portfolios built over time provide growth and income streams that can significantly speed up FatFIRE timelines. This works best with careful market selection and property management.

Commercial real estate, whether through direct ownership or group investments, offers passive income with cash returns of 8-12% plus appreciation. This creates substantial wealth with less time commitment.

Real estate professional tax status provides exceptional advantages for high earners. Potentially, your regular job income can be offset with paper losses while building a portfolio that generates tax-advantaged income in retirement. This strategy requires meeting specific IRS requirements but can dramatically accelerate wealth building for those who qualify.

For more information about how to retire early and other helpful tips, you should check out some of my other articles on the subject:

- How To Retire Early (4 Strategies To Retire Years Ahead of Schedule)

- Using a Roth Conversion Ladder to Retire Early

Investment Approaches For FatFIRE

As your wealth grows, your investment strategy typically becomes more sophisticated.

Build a diversified portfolio for higher returns

Beyond basic index funds, many FatFIRE investors include small-cap value stocks, emerging markets, and real estate investment trusts to enhance long-term returns while staying diversified. These additional asset classes can provide higher returns and reduce overall portfolio volatility through diversification.

One example of a diversified FatFIRE portfolio might look like this:

- 40% US total stock market index fund

- 20% International developed markets index fund

- 10% Emerging markets index fund

- 10% Real estate investment trusts (REITs)

- 10% US small-cap value index fund

- 10% US total bond market index fund

This is just one possible allocation, and your portfolio should reflect your risk tolerance, time horizon, and specific financial goals.

Alternative investments, such as private equity, venture capital, and angel investing, become available at higher levels of wealth. These can boost returns while adding different types of assets to the portfolio. Once your net worth exceeds $1-2 million, you might consider allocating 5-10% to these alternative asset classes.

Directing business investments through minority stakes or silent partnerships allows wealth builders to utilize their industry expertise for potentially higher returns than those in public markets. A physician might invest in a medical device startup, while a software engineer might fund promising technology companies where they have a deeper understanding of the market.

For the simplest, beginner-friendly steps, read my article, Lazy Portfolios You Can Build Right Away (+ How It Works).

Balance growth and wealth preservation

As you approach FatFIRE targets, gradually shift from growth to preservation strategies. Move from 80-90% stocks toward 50-70% to reduce the risk of bad market timing. This transition should typically start 3 to 5 years before your planned Fat FIRE date.

Bond ladders, CDs, and treasury investments create stable income that prevents forced selling during market downturns. This is key for those living off investment returns. A bond ladder with maturities spread across 1 to 10 years can provide a predictable income, regardless of interest rate changes.

Cash reserves of 1-2 years of expenses provide security and spending flexibility. This enables FatFIRE retirees to maintain their chosen lifestyle regardless of market conditions. Having $200,000 to $400,000 in cash or cash equivalents means never having to sell investments during a market downturn.

Planning Your FatFIRE Lifestyle

Financial planning is only half the equation. Creating a fulfilling life in FatFIRE retirement requires thoughtful preparation.

Create a post-retirement vision

If you’re serious about FarFIRE, you should develop detailed visions of their ideal days, weeks, and years beyond financial targets. Think about activities, relationships, and environments that bring you fulfillment.

If it helps organize your thoughts, write down a detailed description of your ideal day in retirement, including where you wake up, who you're with, and how you spend your time.

Another option is to try a "retirement practice run." Taking extended breaks or moving to part-time work before fully retiring helps test and refine their post-career lifestyle.

The main idea is to build plans around core values and interests rather than just increasing spending. This ensures that your financial freedom leads to genuine life satisfaction. If family connection is a core value, your FatFIRE plan might include a second home large enough for family gatherings or a travel fund for visiting distant relatives.

Maintain purpose and meaning after FatFIRE

Many retirees find that purpose becomes more important than leisure once basic enjoyment needs are met.

Board positions, mentorship roles, and advising opportunities allow FatFIRE retirees to use their professional expertise. These roles maintain flexibility and avoid full-time commitments.

Philanthropic involvement through foundations, donor-advised funds, or hands-on nonprofit work provides meaningful engagement and creates a positive impact in the community.

Creative pursuits flourish in a FatFIRE retirement when time constraints and income pressures are gone. Writing, art, music, and craftsmanship often become central to identity and purpose. The financial security of FatFIRE allows you to pursue your creative interests and ensures you’re still feeling fulfilled.

Travel and luxury experiences in retirement

With FatFIRE resources, long-stay international travel becomes possible. This allows more profound cultural experiences through month-long rentals rather than rushed week-long vacations. Spending six weeks in a Tuscan villa gives you time to become a temporary local.

First-class flights, luxury cruises, and premium accommodations transform travel from a stressful necessity to a genuine pleasure. This becomes particularly valuable as physical stamina decreases with age.

Exclusive experiences become accessible. Private guided tours, cooking with famous chefs, or attending premier cultural and sporting events offer memories and connections that typical tourism cannot match. These international experiences are what attract tons of travel-loving people to FatFIRE in the first place.

Manage family wealth and legacy planning

As wealth grows, many FatFIRE achievers begin thinking about impact beyond their lifetimes.

Passing wealth between generations becomes important at FatFIRE levels. Many people establish trusts, family limited partnerships, or other structures to transfer assets to their heirs efficiently. These legal structures can provide tax advantages while ensuring your wealth is used according to your wishes.

Family governance and financial education become priorities. You can also deliberately teach the next generation about money management, investing principles, and values-based decision-making. Regular family meetings to discuss values and financial decisions help prepare heirs to handle inheritance responsibly.

FatFIRE Is Achievable For Everyone, But Balance Is Important

While FatFIRE offers tremendous benefits, it's crucial to maintain perspective and balance throughout the journey.

Finding your personal definition of "enough"

Knowing when you've reached "enough" is perhaps the most challenging aspect of the FatFIRE journey.

Many high-net-worth individuals struggle with "moving goalposts syndrome." Reaching financial targets fails to bring satisfaction and simply leads to setting higher targets. When $3 million was once the dream, reaching it often shifts the target to $5 million, then $10 million, in an endless pursuit of more.

Setting clear "contentment thresholds" with concrete lifestyle descriptions helps prevent the endless wealth pursuit.

What happens when you don’t define “enough”

Chris and Amy's story reveals how even substantial wealth doesn't automatically fix money anxieties. Despite their $8 million net worth, they remain trapped in patterns of excessive optimization, spending hours debating flight routes and hotel choices rather than focusing on the experience itself.

| Chris: [00:02:41] We’re planning a trip, and we’re trying to book flights, and we’re optimizing to a degree that many would think was crazy. And we’re thinking about, which hotel do we stay at? Which flight do we take? Do we leave early? Do we change which island we want to go to, because it’s cheaper to fly to this other one? And I don’t know. We probably, combined, spent-

Amy: [00:03:10] Too long. Chris: [00:03:11] Like five, six more hours in the last 24 hours, Ramit Sethi: [00:03:16] Five or six hours together in the last day. |

Their story highlights a crucial lesson: without defining what "enough" looks like, even multi-millionaires can fall into the trap of endless optimization. For Chris and Amy, spending half a day debating how to save a few hundred dollars on a vacation reveals that money isn't the problem. What's missing is a clear framework for when to optimize and when to simply enjoy their wealth.

Balancing high earnings with quality of life

Pursuing FatFIRE through high-income careers often creates tension with family time, health, and personal interests during key earning years. Consider the psychological toll it might have on you and your relationships.

A 70-hour workweek might accelerate your timeline but could cost you irreplaceable years with growing children or damage your health.

When budgeting and planning for FatFIRE, do so with a clear plan. For example, organizing and following your "money dials" can give direction and help you budget with minimal sacrifices. Money dials are the spending categories that bring you the most joy, like travel, experiences, or convenience, which you turn up while cutting back on things that matter less.

Real-life example of wealth interfering with quality of life

Nicole and Michael's situation demonstrates how the pursuit of wealth can create unexpected emotional burdens even after achieving financial success. With a $5.7 million net worth, they should feel secure, yet Nicole experiences intense anxiety about even minor expenses.

| Ramit Sethi: [00:04:52] Okay. To ask the question that all of us are wondering, is $1,000 really going to make a difference in your financial plan for the rest of the year?

Nicole: [00:05:05] It probably wouldn’t make a material difference, but we’re so close to hitting that goal. And, for me, if we hit it, I feel financially secure. If we don’t hit it, even if it’s by $1,000, I feel really bad. Like, I agonize over it. Ramit Sethi: [00:05:22] Yeah. I mean, you’re an accountant, you know the mathematical answer to my question. What is it, yes or no? Nicole: [00:05:28] No. The answer is no. I wouldn’t change anything. It’d be a rounding error. Ramit Sethi: [00:05:34] Correct. Would it even be in the ballpark of materially affecting your financial goal? Nicole: [00:05:39] Not at all. Ramit Sethi: [00:05:40] Correct. Nicole: [00:05:40] Spending money makes me so, so nervous. It makes me feel like if we even spend, like, $1,000, we’re moving our wealth in the wrong direction. And this is illogical, but spending any amount of money, I feel like we could lose it all. We could lose financial security. We could lose everything we built. We wouldn’t have the money to house our children. We wouldn’t have the money to buy food. We wouldn’t have the money to provide them the life that we want to provide them. They’d have a really rough life, like what I had growing up. |

Their story shows how deeply ingrained money fears can persist regardless of your net worth. For Nicole, the psychological impact of her childhood financial insecurity continued to dominate her thinking despite their multimillion-dollar wealth.

Avoiding the "more is always better" mindset

I recommend optimizing life quality rather than maximizing net worth. There are diminishing returns on happiness beyond certain wealth thresholds. Research suggests that while money does buy happiness up to an annual income of about $75,000 to $95,000, the effect diminishes significantly beyond that point.

Research consistently shows that experiences, relationships, and purpose drive life satisfaction far more than consumption or account balances beyond middle-class comfort levels. The joy from meaningful connections and engaging activities usually outweighs the pleasure of luxury possessions.

Should FatFIRE Be Your Goal?

FatFIRE isn't right for everyone. Consider carefully whether this path aligns with your deepest values and priorities.

Assessing if FatFIRE aligns with your values

Take time to reflect on what truly matters to you before committing to the FatFIRE path.

Clarify your true priorities through exercises like "ideal day" visualization or ranking your values. This helps determine whether the luxury retirement of FatFIRE aligns with what brings you joy. Write down in detail what your perfect day would include, then analyze how much of it requires FatFIRE-level wealth.

Some find that premium versions of activities they genuinely love justify FatFIRE pursuits. Others discover their happiness comes from simpler pleasures that don't require massive wealth. If your greatest joys come from reading, hiking, and time with family, traditional FIRE might serve you better than FatFIRE.

If you don't want or need a luxurious lifestyle, achieving FatFIRE might not be worth the long-term sacrifices usually necessary. The extra years of work required might outweigh the incremental benefits of higher spending in retirement.

Recognizing when traditional FIRE might be enough

For many, the standard FIRE approach provides sufficient resources for a fulfilling life.

Standard FIRE, with $1-2 million invested, can provide substantial freedom and a modest level of luxury for those who don't have expensive tastes or location constraints. This level of wealth can fund a comfortable, middle-class lifestyle indefinitely with proper management.

Geographic flexibility dramatically impacts required numbers. Traditional FIRE might fund a lifestyle abroad that would require FatFIRE levels in the United States. A $2 million portfolio that provides a modest lifestyle in San Francisco could fund a luxurious life in many international destinations.

Considering the sacrifices required for FatFIRE

The path to FatFIRE often involves significant tradeoffs that should be carefully weighed.

Career choices optimized for income often involve lifestyle tradeoffs. These include stress, extensive travel, long hours, and limited location flexibility during prime earning years. High-earning careers usually require sacrifices in other areas of life, which may or may not be worth the financial rewards.

Family relationships, health maintenance, and personal interests need protection during periods of intense earning. These well-being foundations cannot be purchased later if neglected. No amount of wealth can buy back time not spent with growing children or restore health damaged by chronic stress and overwork.

Example of how the sacrifices and mindset are truly not for everyone

Gavin and Carolyn's experience shows how an extreme focus on financial independence can lead to unhealthy relationships with money. Their pursuit of FIRE led to behaviors that even Gavin's brother called out as "ridiculous" and "cheap."

| Ramit Sethi: [00:12:43] That’s my special help. Gavin, how did you get from the FIRE community to meet because the FIRE community loves their receipts?

Gavin: [00:12:53] Basically, I tried to get everyone around me involved in the FIRE community. Ramit Sethi: [00:12:57] Oh, wow, that must [inaudible 00:12:58]. Gavin: [00:13:02] I got good reception in some places and not such good reception in other places. But really it was my brother. He’s like, “You’re ridiculous. You’re out of control.” He didn’t say you’re cheap. But that– Carolyn: [00:13:18] Oh no, he did. He definitely said that. Gavin: [00:13:24] And he kept suggesting that I read your book, and I just wasn’t into it. And finally, when the podcast started coming out, he said, “You should listen to this podcast.” And I did and I had already started to change my perspective a little bit. But I think the podcast and reading the book solidified it for me. |

Their journey highlights how the pursuit of FIRE can sometimes cross from financial discipline into unhealthy restriction. This demonstrates why balance is crucial on the path to financial independence, whether you're pursuing standard FIRE or FatFIRE.

Defining your Rich Life beyond just the numbers

Define wealth holistically, encompassing health, relationships, purpose, experiences, and financial metrics. A Rich Life balances all these elements rather than maximizing any single one. Consider what a Rich Life means to you personally:

- A Rich Life means having control over your time and energy, allowing you to direct both toward what matters most to you, whether that's family, creative pursuits, community involvement, or leisure.

- A Rich Life includes meaningful relationships and connections that provide emotional support, joy, and a sense of belonging that no amount of money can replace.

- A Rich Life balances present enjoyment with future security, allowing you to savor today while confidently planning for tomorrow without excessive worry or restriction.

Freedom of time and choice consistently ranks above luxury consumption as the primary motivation for FatFIRE pursuers who maintain satisfaction after achieving their goals.

Creating a detailed vision of your Rich Life, with specific activities, environments, relationships, and contributions, provides a more meaningful target than arbitrary net worth goals.

Stay in the know

Be the first one to receive new releases,

special offers, and more