LLC tax filing: What you need to know as a solo entrepreneur

When you work for a company, a lot of tax stuff is just taken care of. Your company takes a certain percentage out of your paycheck every pay period. Adjustments for things like healthcare and retirement contributions get made automatically. In most cases, you don’t even miss the money, because you never see it to begin with.

When you strike out on your own and start your own business, suddenly you ARE the boss, and all of that stuff that just sort of happened at your job — like taking taxes out of your paycheck — it’s your job to figure all of that out.

One way to bring some order to the chaos? Set your business up as an LLC.

“LLC” stands for “limited liability company.” Basically, it’s a way of labeling your business so that when it’s time to pay taxes, the government knows how much to charge you and what to do with your money.

LLCs are a popular option among entrepreneurs because they’re the Hannah Montana of the tax filing world: they give you the best of both worlds.

You get:

- The advantages and protections that the IRS gives businesses. For example, if customers are unhappy with your business, they can’t sue you — they can only sue your business.

- The simplicity of paying taxes as an individual. You just pay estimated quarterly taxes like a freelancer, and then report your business income on your individual 1040 at the end of the year.

When you set yourself up as an LLC and start paying taxes, it’s like a coming out party for your business. It’s a way of saying “Here I am! I am a business owner, and I am ready to be taken seriously as the kickass entrepreneur that I am.”

That’s pretty amazing, if you think about it. Operating agreements and quarterly tax deadlines and 1040s and all.

5 steps to paying taxes as an LLC

- Create an LLC, if you haven’t done so already.

- Open a separate business bank account for all business earnings and expenses.

- Set aside 30-40% of all business earnings for taxes — and DO NOT touch that money unless it is to pay taxes.

- Pay your estimated quarterly taxes four times each year at www.irs.gov.

- At tax time (April 15th or before for the previous fiscal year), report your business’s total income by filling out a Schedule C form and filing it with your 1040.

DISCLAIMER: Every business is different. This post will give you an overview of what goes into setting up and filing taxes for a sole-member LLC. But if you have any questions about your specific situation, your best bet is to find a good tax attorney in your area who can help you work through the specifics of your business.

How do you find a tax attorney?

Ask for a referral from someone you trust — maybe a fellow business owner, or the banker, lawyer, or accountant you work with. If you can’t get a referral, inquire directly at the local bar association in your area.

Check their qualifications. Before you hire any attorney to consult for your business, confirm that they:

- Have a JD

- Are licensed to practice law in your state

- Specialize in tax law

- Have a proven track record of working with solo entrepreneurs and small business owners

Wait a minute: Do I even need to be here?

Hold up: tax attorneys, operating agreements, a whole alphabet soup of form names … At this point, you may find yourself wondering: do I even need to worry about this yet?

In all honesty, the answer may be “no.”

At IWT, we’re big believers in worrying about the right things at the right times. And worrying about creating a business entity for a business you’re not even entirely sure will exist yet? That’s putting the cart way before the horse.

Our advice: worry about earning revenue from actual paying customers before you worry about what to do with that revenue. Quarterly tax filing requirements don’t even kick in until you clear $1,000 in revenue anyway.

Focus on earning that first $1,000. Maybe add on the cost of filing an LLC in your state to begin with, that way the cost of setting up pays for itself.

If this is you, bookmark this post and come back to it.

For those of us still here, let’s dive into how you set up and pay your taxes as an LLC.

What does an LLC do?

When you create an LLC for your business, what you’re essentially doing is establishing your business as its own person. Let’s call this person “Biz.”

Biz has her own bank account (more on that in a second). She has her own income that goes into that bank account. From a tax and legal perspective, Biz is a separate entity. You, the entrepreneur, are just the owner (or, in legal terms, the “manager”) of the LLC. You’re like the executor of Biz’s estate.

Some specific advantages that gives you:

It protects your personal assets. This is the #1 most important thing that creating an LLC does for you as an entrepreneur: protect your personal assets in the event of a catastrophe. It’s right there in the name LLC — “limited liability company.” Your liability as the business owner is limited by the legal protections of your LLC. Should the worst happen — an unhappy client sues you, or your business goes into debt — the assets that belong to your LLC are the only things the lawyers or debt collectors can touch. It’s Biz’s problem, not yours. Your personal assets — like your home, your emergency fund, your retirement savings, or your child’s college fund — are protected.

It keeps your business and life separate. When you establish your business as its own separate entity, you get used to thinking about it as its own separate entity. If you get used to thinking of your business’s money as your business’s money, not yours, it changes how you think about that money. Think about it: whose money are you more likely to spend — yours, or somebody else’s? When you see $1,000 worth of profit sitting in your business checking account, what are you more likely to do — send it to your personal account so you can buy that dope skateboard, or whatever it is that kids spend their money on these days? Or reinvest it back in your business?

Step 1: Set up an LLC

The first step to paying taxes as an LLC is to … well, set up an LLC.

This is a big topic — one that warrants a post all to itself. In broad strokes, though, here are the steps you need to follow:

Steps to forming an LLC

- Give your LLC a name. This will need to be unique in your state. Before you move forward with registering your LLC, you should confirm that the name you want is available through the Secretary of State for your state.

- Appoint a registered agent. In most states this can be anyone over the age of 18 (including yourself) who is responsible for handling any and all correspondence on behalf of the LLC.

- File the necessary paperwork (usually called “Articles of Organization”).

- Create an operating agreement. You can download free templates around the internet, or work with an attorney to design an operating agreement that you feel comfortable with.

- Get your Federal Tax number (EIN). Note: if you set up your LLC as a single-member LLC, you’ll skip this step and use your personal Tax Identification Number (TIN).

Useful link: More information on setting up an LLC

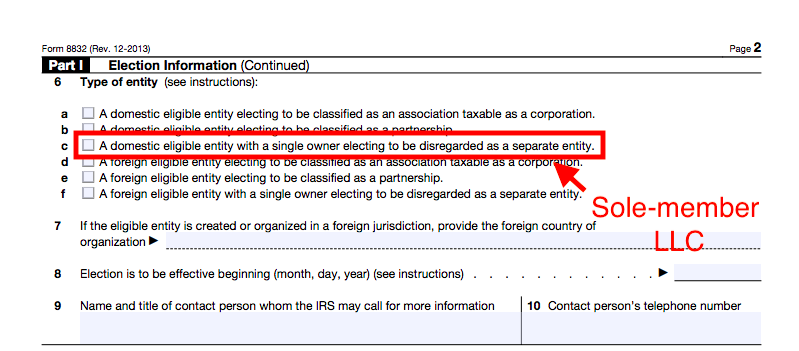

There are three separate types of LLCs — each with specific tax rules. When you set up your LLC, you’ll need to designate how you want to be taxed by filling out Form 8832.

Your options are:

- Sole-member, where you, the business owner, are the sole owner of the LLC and assume all responsibility for paying taxes related to your business.

- Partnership, where you co-own the business with at least one other person, and split the business profits and expenses between you for tax purposes.

- Corporate, where you’re setting up as a full C or S corporation and electing to be taxed.

Important form: Form 8832

For the purposes of this article, we’re going to assume that you’re a solo entrepreneur setting up as a sole-member LLC. If a partnership or corporate LLC is more what you’re thinking about, just be aware that some of the advice in this article may not apply.

Useful links

More information about single-member LLCs

More information about filing as a corporate or partnership LLC

Warning: Watch out for hidden LLC fees

One thing to note upfront: there are costs associated with setting up an LLC. LLCs are regulated at the state level, so the costs and specific requirements for setting up an LLC vary from state to state. The average state filing fee to form an LLC is $127, with the majority of the 50 states falling somewhere between $50 to $150, according to data from LLC University.

Forms, fees, and additional information about forming an LLC in your state can be found on the website of your Secretary of State.

Useful link: More about state-specific LLC fees and requirements

Step 2: Open a separate bank account for business expenses

Once you’ve established your business as its own separate person by creating an LLC, the next step is to give it its own separate expenses by creating a dedicated business bank account.

We’re not talking about just any checking account — banks have dedicated accounts for businesses. The day you set yours up, you’ll need to show documentation of your LLC, including:

- LLC approval — your LLC’s approved Articles of Organization, which might be called something different in your state (Certificate of Formation or Certificate of Organization).

- Your Federal Tax ID Number (aka EIN). You’ll get this when you create your LLC.

- 2 forms of identification including a government-issued ID (like a driver’s license) and a credit card, passport, voter’s registration, or utility bill.

- Your LLC’s operating agreement and additional forms required by your state.

Keeping your business account separate from your personal one is important for a couple of reasons: #1 being that it establishes the limited liability that we talked about already. The whole reason that you’re able to claim that your personal assets and your business assets are separate is because the expenses all live separately. If you start intermingling personal accounts with business accounts, that’s where you open yourself up to being held personally accountable for what happens in your business.

So, purely from a legal perspective, it’s important to keep that firewall firmly in place: business accounts over here, personal accounts over there.

But there are some additional, practical benefits to keeping business money and personal money separate — especially come tax time.

- Keep track of spending. If all of the earnings and expenses for your business are flowing in and out of this one account, it makes it that much easier to track how much exactly your business is spending.

- Calculate income and for tax purposes. Clearly delineated business spending also makes it easier to track how much your business owes in taxes — and how much you can write off in the form of business expenses.

Useful link: Opening a business bank account for your LLC

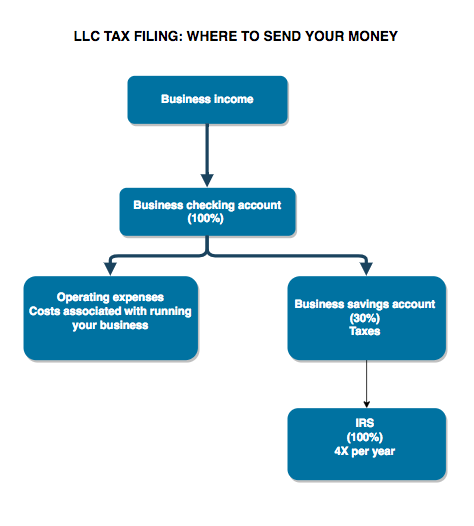

Step 3: Pay the government first (by setting tax money aside)

Once you have your business account set up, be sure to reroute any business earnings to the new account. Then it’s time for the fun part: setting aside taxes so when the due dates come up, you have every dollar accounted for.

There’s a term you hear a lot in personal finance circles: pay yourself first.

The idea is that the best way to make sure you’re on track for your personal goals, like debt repayment and retirement, is to put money toward those goals first — BEFORE you handle bills or allocate yourself “guilt-free” spending money.

There’s a spin on this principle for business owners. It’s called: “Pay the government first.”

The principle is the same: the best way to make sure you’re on track to pay the taxes that you owe the government come tax time is to make paying the government the absolute first thing you do any time your business makes money.

Basically what you’re doing here, by setting money aside, is replicating the process that takes place when an employer withholds taxes from your paycheck.

There are a couple of different ways to track this:

- Per transaction. As soon as a payment hits your bank account, whether it’s a course purchase or a coaching payment, immediately transfer 30% of that payment into your business savings account for taxes.

- Do it if: You’re just starting out, or your earnings aren’t that consistent month to month.

- Per month. Tally up your total business income for the month, then calculate 30% of that and move it over to your savings.

- Do it if: You’re earning enough on a month-by-month basis that it makes more sense to calculate your taxes monthly rather than transaction-by-transaction.

- Per year. If you know roughly what your income is likely to be for the year, you can plan ahead by taking your yearly income, multiplying it by .3 and then dividing that number by 4 to get your estimated quarterly tax payment.

- Do it if: You have an established business with earnings you can use to calculate your likely tax liability.

How much should I aim to save?

This is a short answer to a looong question, but basically: aim to save 30%.

Statistically, if you save 30%-40%, you’re going to likely clear your tax liability including federal, state, and self-employment taxes.

To be clear: this is likely to be a safe estimate. If you’re the kind of person whom it galls to the very core of your being to think of the IRS holding on to money that you could be putting to other use, you can try to get a more accurate calculation of what your tax liability is likely to be.

But if you’re of the “better safe than sorry” mindset, or you’re comfortable thinking of over-paying on taxes as a “loan” that you’re giving to the government — 30% is a good benchmark to aim for. It’s better to oversave than to find yourself scrambling to come up with the money you owe at the very last second.

Note: When you’ve been in business for a while, you can start to use your income history as a blueprint for how much to save. For example: “I earned $60K from my business last year, and I paid $18K in taxes. I’m on track to earn the same this year, so I’m going to save the same amount.”

The most important thing to remember about setting money aside for taxes: Once you set money aside in your tax account, it is GONE. DEAD to you. You’re like a host in Westworld: programmed to ignore the things that might hurt you.

When you see that money accumulating, it’s tempting to start thinking you can borrow it and replace it later. But tapping your tax fund for a “quick expense” here or just to “bridge the gap” there is a slippery slope that can lead to you turning out your pockets come tax time and wondering, “Where did the money go?”

Once the money goes into your tax savings account, it’s not your money. It’s the government’s money. You’re just holding on to it for them until it’s time to hand it over. Which brings us to our next point…

Step 4: Pay taxes quarterly

As long as you’ve been consistent about setting aside your 30% for taxes as you earn it, this next step is relatively straightforward: once a quarter (every three months), you just take the money in that savings account and send it to the government.

The IRS provides a handy (and unchanging) calendar for when quarterly taxes are due each period:

| For the pay period spanning: | Quarterly taxes are due on*: |

| January 1 – March 31 | April 15 |

| April 1- May 31 | June 15 |

| June 1 – August 31 | September 15 |

| September 1 – December 31 | January 15 (of the following year) |

*Note: If the due date listed falls on a Saturday, Sunday, or legal holiday, the payment is considered “on time” if it’s mailed/submitted on the first business day after the weekend or holiday.

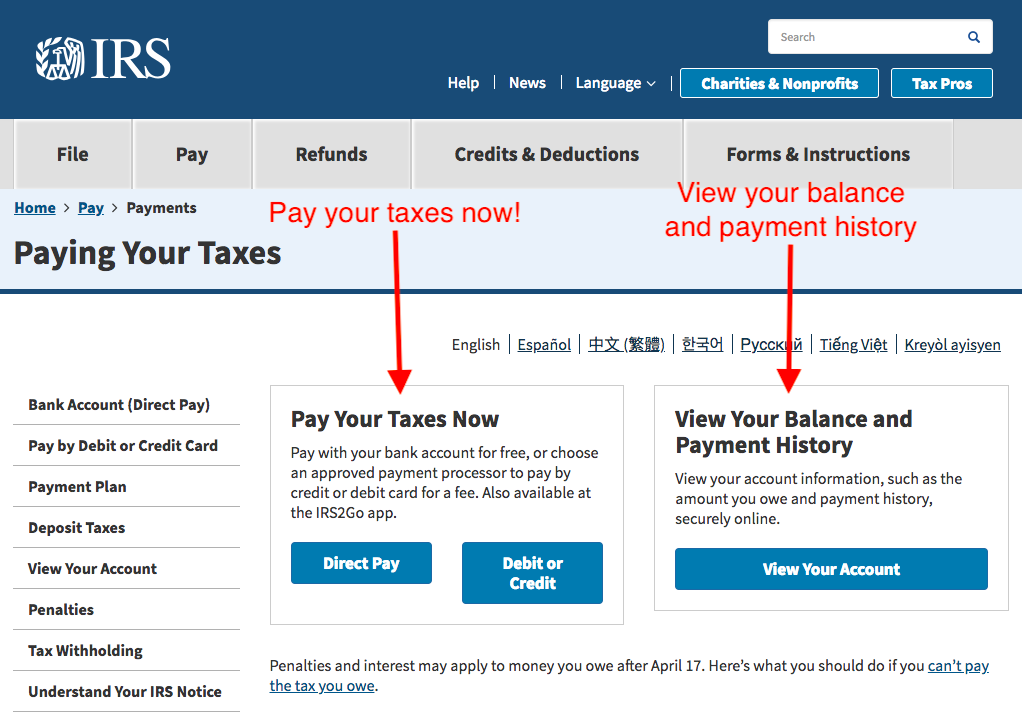

How do I pay my quarterly taxes?

The good news here is that technology has caught up with the contemporary solopreneur: You can pay your quarterly taxes directly on the IRS website — and it only takes a few minutes.

Here’s how to do it:

- Go to https://www.irs.gov/payments

- Select “Direct pay” or “Debit or Credit” under “Pay your taxes now.” (We’d recommend direct pay to spare yourself some unnecessary fees.)

- Follow the instructions to pay the amount that has accumulated in your tax savings account for the period.

- Save your receipt and any other communications you receive to a dedicated folder, so that in case there are any questions, you have your “paper trail” ready with documentation to show what you paid when.

Tool tip: If mobile is more your speed, you can download the official IRS app, IRS2Go, and make your payments there.

“I missed a quarterly tax deadline! What do I do?”

First, you must walk the streets barefoot wearing a sign that says “I’m a dirty tax evader.”

Just kidding.

If you miss a quarterly tax payment, it’s not the end of the world — but you do want to make it a priority to catch up sooner rather than later to avoid late fees from our friends at the IRS.

Don’t wait until the next quarterly deadline hits, because there are late fees, and they stack up. Settle up the best you can as soon as you can.

Step 5: Tax time

Finally, it’s here — April 15: tax time.

In a weird bit of tax logic that only tax lawyers can explain, the government considers your business to be its own separate entity — until tax time rolls around. Once April 15th hits, you just report your business earnings on your personal tax form.

You have heard the term “pass through organization”: this is what people are talking about when they use that term. The profits of the business “pass through” the LLC to the individual members of the LLC. So if you’re the sole member of a sole-member LLC, all of the profits pass through to you, and you report them on your personal tax form.

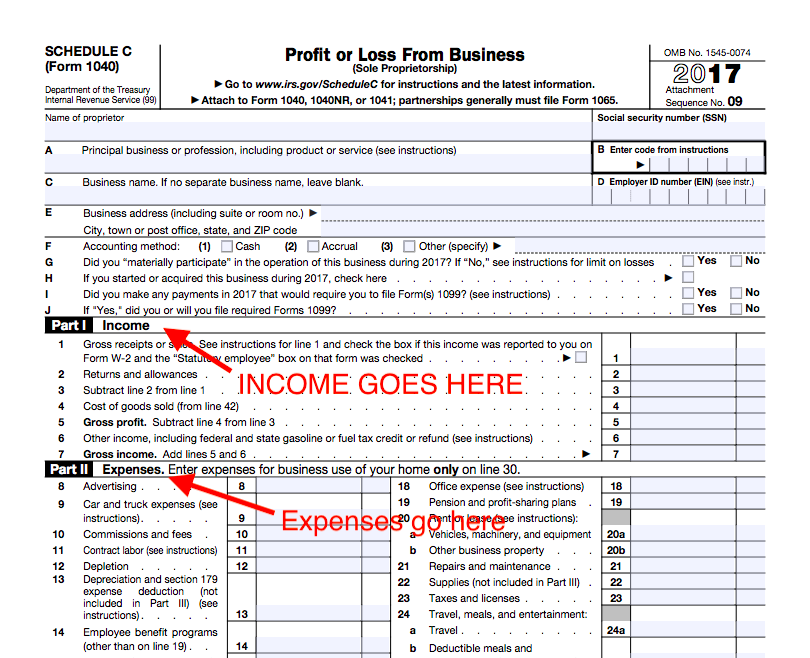

So when you’re preparing your personal income tax return, you complete a Schedule C attachment to your 1040 (your individual income tax return). The Schedule C reports the income and deductions that relate to your business activities.

This again, is why setting up a separate bank account from the beginning is key: if all of your business earnings and expenses are flowing in and out of that one bank account, tallying up come tax time isn’t all that much of a chore.

Deductions

Yayyy, the fun part! Because, as an LLC, you are a business, the IRS will let you deduct expenses associated with running your business. It’s kind of like the way you can deduct retirement savings and health insurance costs from your personal taxes. The government wants you to grow your business — so they make it worth your while by giving you a discount on the activities that help you do it.

Interesting to note: the IRS considers expenses deductible if they are “both ordinary and necessary.” That means the expenses don’t have to be “indispensable” to the business — just one that is commonly accepted in your field of endeavor.

In other words: be generous when you list out your deductions. Your post tax-day self will thank you.

Things that count as deductions:

- Home office space (itemized as a % of your rent or mortgage)

- Internet

- Gas/transportation for work-related travel

- Web hosting and other expenses

- Services (such as design or virtual assistant services)

Important link: The IRS’s page on deductible business expenses

Last (but definitely not least): Get help if you need it

There you have it: all the basics you need to know about filing taxes as an LLC.

As a reminder, while it is possible to handle all of this stuff on your own, it can be worth working with a professional tax attorney and/or accountant to ensure everything. An attorney can help with making sure your forms are in order and you’ve selected the right designation for your business goals. And a tax professional can help you make sure you’re setting enough aside and making the most of your deductions.

Creating an LLC for your business is an investment in your future — both as a business owner and as an individual. It’s worth taking the time to get it right.