What Are Mutual Funds and How Do They Work: All The Basics

Thats it! No front- or back-loading fees, and no money manager who might screw up your investments. Just the opportunity for you to invest directly into the market.

Many brokers such as Schwab also have index funds that invest in an international market as well as the 1,000 largest publicly traded companies in the United States.

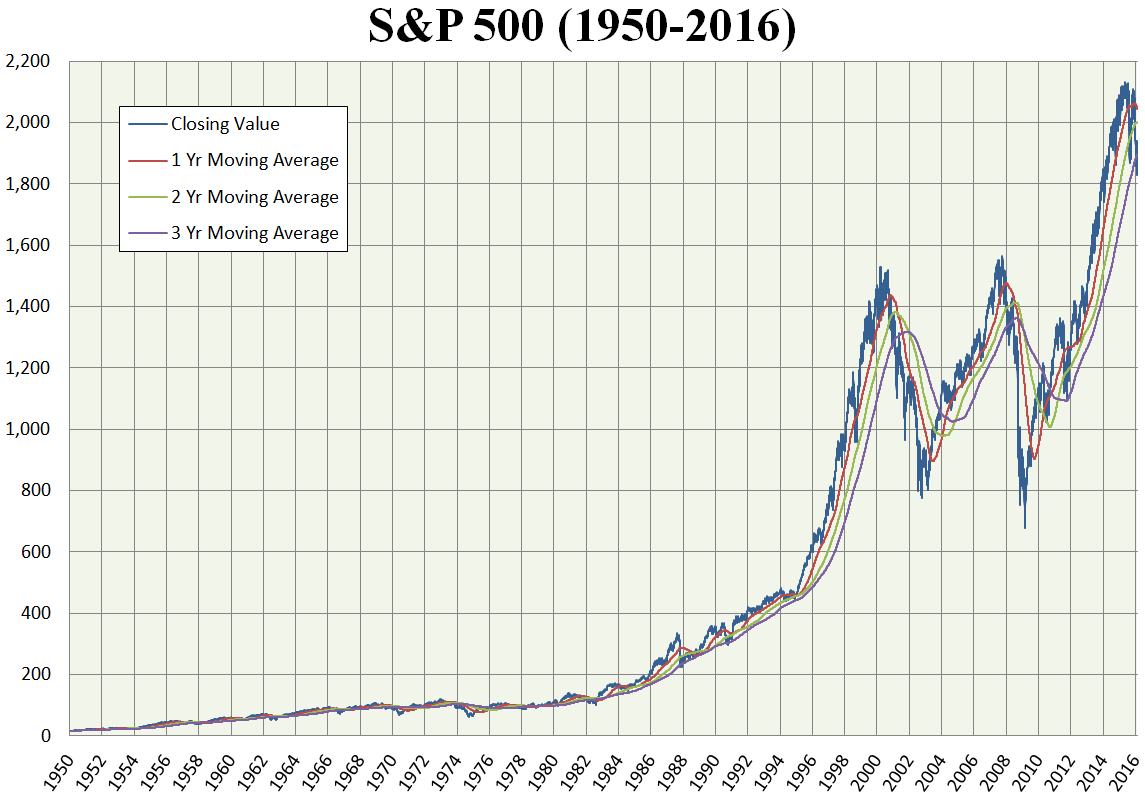

Since index funds invest in the entire market, theyll be less volatile which means youll earn money slower. But if you keep your money in the market over your lifetime, I promise you youll make money.

I LOVE index funds and Im in good company:

[Most investors would] be better off in an index fund. -Peter Lynch

Just buy the damn index funds. -John Bogle

Consistently buy an S&P low-cost index fund. Its the thing that makes the most sense practically all of the time.”

There’s a reason index funds are a favorite of financial leaders and thinkers out there. Its because they WORK.

So lets recap. Again.

Advantages of index funds:

- With less risk, you stand to make a lot more money with index funds.

- You save money on dumb costs because index funds dont have money managers or sales-loading costs. Your expense ratio is also much lower.

Disadvantages of index funds:

- Slower gains in funds.

- Thats it.

Okay, Im sold. How do I invest in a mutual fund?

When it comes to actually purchasing a mutual fund and investing, I suggest two places.

Roth IRA and 401k

Your retirement accounts (Roth IRA and 401k) let you purchase index funds. To do so through your 401k, youll have to speak to your companys HR department to set up an investment plan through the mutual fund you want. And, as Ive written, the S&P 500 index fund is a great place to start.

If you want to invest through your Roth IRA, youll have to set it up through a brokerage.

Check out my video below, where I suggest a few good ones to help you get started with your Roth IRA.

Banks, credit unions, and stockbrokers (oh, my!)

Banks, credit unions, and stockbrokers offer avenues to invest in mutual funds. In fact, there are plenty of fantastic brokers that offer a wide variety of mutual funds for you to choose from.

My suggestions:

- Vanguard (This is the one I use)

Phone #: 877-662-7447 - TIAA

Phone #: 800-842-2252 - Charles Schwab

Phone #: 800-435-4000

All of these places offer an excellent variety of index funds to choose from, so you cant go wrong with them.

Signing up is ludicrously easy. Just follow the 7-step guide Ive outlined below (the wording and order of the steps will vary from broker to broker but the steps are essentially the same).

NOTE: Make sure you have your social security number, employer address, and bank info (account number and routing number) available when you sign up, as theyll come in handy during the application process.

- Step 1: Go to the website for the brokerage of your choice.

- Step 2: Click on the Open an account button. Each of the above websites has one.

- Step 3: Start an application for an Individual brokerage account.

- Step 4: Enter information about yourself name, address, birth date, employer info, social security.

- Step 5: Set up an initial deposit by entering in your bank information. Some brokers require you to make a minimum deposit, so use a separate bank account to deposit money into the brokerage account.

- Step 6: Wait. The initial transfer will take anywhere from 3 to 7 days to complete. After that, youll get a notification via email or phone call telling you youre ready to invest.

- Step 7: Log into your brokerage account and start investing!

The application process can be as quick as 15 minutes. In the same time it would take to watch half an episode of Rick and Morty, you can be well on your way to financial success.

If you have any questions about funds or trading, call up the numbers provided above. Theyll connect you with a fiduciary who works for the bank to give you the best advice and guidance they can.

Beyond Mutual Funds

If you want even more actionable tactics to help you manage AND make more money, youre in luck. I wrote a FREE guide that goes into detail on how you can get started doing just that.

Join the hundreds of thousands of people who have read it and benefitted from it already by entering your information below to receive a PDF copy of the guide.

When youre done, read it, apply the lessons, and shoot me an email with your successes I read every email.

Ramit Sethi

Host of Netflix’s “How To Get Rich” NYT Bestselling Author, & Host of the I Will Teach You To Be Rich Podcast. I’ll show you how to take control of your money with my proven strategies so you can live your RICH LIFE.