How to Lower Your Credit Card Interest Rate (Scripts Included)

The exact script to lower your credit card interest rates

Since the average APR is typically somewhere between 12% and 15%, it can be extremely expensive to carry a balance on your card.

Think of it like this: The average long-term return on investments in the stock market is around 8%. If you could get a 14% return on your investments, you’d be thrilled!

That’s exactly what credit card companies all over the world are doing. You want to avoid the black hole of credit card interest payments so you can earn money — and not give it to the credit card companies.

That’s why you should call your credit card company and ask them to lower your APR.

Here’s a simple script you can follow to help you.

YOU: Hello, I’d like to lower the APR on my credit card, please.

CREDIT CARD REP: Umm…why?

YOU: I’ve been a loyal customer to you for X years. Also, I’ve paid my bill in full and on time for the past few months. I know a few other credit cards offering better rates than what I’m getting right now, and I’d hate for this interest rate to drive me away from your service. What can you do for me?

CREDIT CARD REP: Hmm. Let me check…Mr. Sethi, I just discovered that I can lower your rate from 15% to 12%. Will this work?

When the conversation is finished, follow these three very important steps:

- Step 1: Hang up the phone.

- Step 2: Hold up one hand above your head.

- Step 3: Use your other hand to high five yourself because you just successfully negotiated a lower APR.

This is a quick and easy way to get a Big Win with one phone call, BUT it’s also completely unnecessary.

BONUS: If you want even more tactics you can use to optimize your credit cards, check out the 2-minute video below, which was recorded in approx. 1976.

It’s important to note: Your credit card interest rates don’t matter. I’ve gotten some heat for this idea but I don’t care. At the end of the day, it shouldn’t matter how much your APR is.

Why it doesn’t matter if your credit card interest rate is 20% or 80%

It’s simple: I never carry a balance on my credit card — and neither should you. When it comes to making purchases, if I can’t pay it off at the end of the month, I don’t buy it.

Let’s say you have a $10,000 balance on your credit card and you pay the minimum amount, which is around 2.5% every month. How much will it actually cost you? The answer is shocking. Get ready!

If you only paid the minimum on your $10,000 balance, it would take you 452 months (over 8 years!) and cost you over $19,000 in interest alone.

In other words, you’d pay around $30,000 for a $10,000 balance.

That’s if you just pay the minimum monthly payment. How about if you pay the same amount every month so that you pay down the balance faster over time?

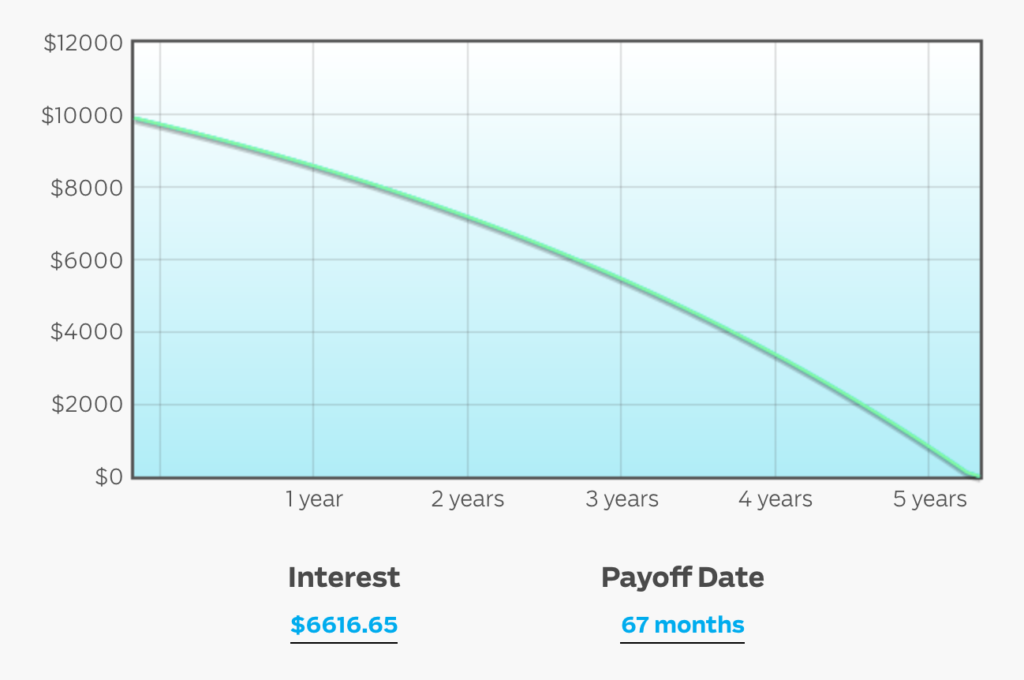

Let’s take the same $10,000 balance and pay $250 off every month.

It will cost you more than $6,000 in interest and take you 67 months to pay off the balance. Even if you don’t buy another thing in that time!

This is why credit card companies are so incredibly profitable, especially with young people who don’t know any better.

The point is pretty obvious:

- Don’t carry a balance (if you do, pay it off as quickly as you can).

- Pay the maximum possible on your balance every time.

- If you can’t pay off a purchase by the end of the month, don’t buy it.

“But Ramit,” people say, “what about homes and college and cars? How can I pay that off in one month?” Yes, true, those very expensive purchases necessitate some kind of longer-term loan. But not with your credit card.

So when I hear people excited about their introductory interest rate (“It’s 0% for 6 months!!”), I’m not really impressed. As long as you pay your balance in full every month, your credit card interest rate is meaningless.

Frequently Asked Questions:

Do you pay APR (Annual Percentage Rate) if you pay on time?

If you pay your credit card bill off on time and in full every month, your APR won’t apply. If you pay your bill on time but not in full, you’ll be charged interest on your remaining balance.

How fast does your credit build with a credit card?

If you pay your bill on time and otherwise manage your finances responsibly, you can rebuild from a bad credit score (300-639) to a fair credit score (640-699) in approximately 12-18 months.