All About Stocks and Bonds: What You Need to Know

Investing is the single most crucial thing you can do to ensure your financial future — and the sooner you start, the easier it is to get rich. There is more than 100 years of evidence in the stock market that suggests this.

Stocks and bonds are a great place to start, so we’re going to dig into that in this post. But first, let’s talk about the typical perceptions of investing.

People still don’t understand what investing is exactly. Folks seem to think there is some magical way to make a fortune with stocks and bonds. From what I’ve seen, the two things people get most wrong about investing are thinking:

- It’s a 24-hour Wolf-of-Wall-Street—style party where traders make millions of dollars daily while screaming “SELL! SELL!!” into a phone.

- Investments are incredibly risky because all the pundits scream “financial crisis!” at even the slightest dips in the markets.

And, frankly, you have every reason to believe this.

Thanks to Hollywood and the (annoying) talking heads on cable news, we’ve come to think of investment as a maniacal creature that’s not suited for the average person… and many of us just don’t understand exactly how investing works.

That’s why we want to dispel some of those myths and notions surrounding investing by focusing on some of the most common topics you’ll hear when it comes to investments:

How do stocks and bonds work? How can you balance them in your portfolio? What’s the difference between stocks and bonds?

This article isn’t going to be about which stocks are hot right now or what sort of investment strategy is going to make you into a zillionaire today. If you’re looking for something like that, I suggest you go back to watching the pundits on cable news.

SPOILER ALERT: Cramer has done much worse than the S&P 500 since 2008.

Instead, stick around for a no-BS lesson all about stocks and bonds, what they are and what part they can play in your investment future.

What is equity vs. debt?

The two types of investment you need to know about are the equity and debt markets. These refer to two different ways investments are bought and sold. In the debt market aka the bond market, investments in loans are bought and sold. In the equity market or stock market, it’s equity in a company that’s bought and sold. Generally, the equity market is deemed a higher risk than the debt market.

How does the bond market work?

The bond market or debt market works by a company taking a loan out. Instead of heading over to the bank, they’ll get that funding from investors who buy bonds.

The company then pays an “interest coupon” which is the annual interest rate paid on a bond.

Bonds fall into either short-term, medium-term, and long-term. Short-term bonds “mature” or are paid off essentially within one to three years. Medium-term bonds last around ten years and long-term bonds mature over much longer periods of time.

Do you earn capital gains on bonds?

Capital gains are what you earn after you sell an asset for more than you bought it for. For example, if you purchase a house and it shoots up in value by the time you sell it, you just made a capital gain. In the stock market, if you sell a stock for a higher price than you bought it, congratulations, you just made a capital gain.

But what about bonds?

Bonds are a little trickier because they’re typically a bit harder to sell than stocks. With bonds, your source of income is related to interest rather than equity income.

Bonds are often not held until they hit maturity and are sold before then. If you do this, you might earn a capital gain (or loss) depending on what has happened to the company that sold you the bond. If you manage to sell your bond for higher than you bought it, this is a capital gain.

How does the stock market work?

The stock market or equity market is a market where the share of ownership in a company is bought and sold.

There are two main ways to make money from stocks—dividends and selling.

Owners of stocks can profit from dividends, a percentage of company profits that shareholders receive. It might be a bit weird to think of yourself as a shareholder… but that’s exactly what you are if you own a stock.

Depending on a myriad of factors, whoever owns stock can also profit when they sell it. But this only works if the market price has increased since you bought it.

The stock market is a bit more volatile than bonds. Stocks can shoot up in value or plummet for a whole range of reasons. Stocks can be affected by social changes, politics, economic events, or even the CEO tweeting (eye roll emoji).

This makes them a riskier investment, but that’s why you need to educate yourself on them. And if you’re still here congratulations!

How should you balance stocks and bonds in your portfolio?

So now we’ve covered the basics of stocks and bonds, the question is: What do you invest in? You can do either stocks or bonds but a mix of the two is a popular choice. It spreads your risk and diversifies your portfolio—something you should always aim for.

But which should you invest more in? The safer, guaranteed but low returns of bonds or the higher risk, higher reward stocks?

Well, there’s no clear-cut answer here. It all depends on…

- Your attitude to risk

- How close to retirement you are

Investment portfolios all fall somewhere on a scale of super aggressive to conservative.

A super aggressive investment strategy would be to put 100% of your money into stocks. A conservative portfolio would have no more than 50% in stocks.

For moderate growth, you’ll want to look at more of a 60/40 split of stocks and bonds.

How does that relate to retirement?

If your portfolio is a key part of your retirement strategy, then the amount of risk you should take depends on how close you are to retirement. In other words, if you’re nearing retirement, you don’t want to dump all your money on high-risk stocks. You’ll want to rebalance your portfolio to be a bit safer and predictable. In this case, you’d probably opt for the more conservative split.

Those who are younger have a bit more flexibility because generally, the more time in the market, the more time your portfolio has to recover if it takes a dip.

How do you start investing in stocks or bonds?

So now you’re all filled in on what stocks and bonds are, how do you start investing in them? As the taste for investing grows, so do the options available to us. Now it’s easier and more accessible than ever. Here are a few popular options to get started:

Use an online brokerage

Possibly the most popular method of investing is to use an online brokerage. This works much in the same way as a traditional in-person broker does but the fees are lower and you can do it all through your smartphone.

Online brokerages let you buy all types of investments including individual stocks, funds, and bonds through a website or app.

Mutual funds

Another popular way to invest is to use a mutual fund instead of investing in individual stocks. Mutual funds are made up of several different companies so the risk of investment is spread rather than targeted and risky.

Unlike many online brokerages, mutual funds typically have a dedicated fund manager who picks the best investments for you. This means they come with much higher fees as a result.

Index funds

Index funds are made up of a group of companies so the risk is spread. The main difference between index and mutual funds is that index funds are passively managed.

This means they’re the cheaper option and they’re also the less volatile option. Rather than trying to beat the market, index funds watch it and make sensible investments.

Robo-advisors

It might sound a bit sci-fi, but it’s pretty simple. A robo-advisor is a digital platform that invests your money through automation and algorithms. There’s little or no human contact involved (great for introverts) so it’s a very hands-off type of investing.

Investment managers

Finally, if you have the cash to splash and want to make some serious investments, hiring a dedicated investment manager is another option. This is the most expensive option as you’ll be getting advice and tailored service. So it’s not ideal for those who want to save money on fees.

IWT’s investment philosophy

When it comes to what you want to invest in, stocks and bonds are both solid investments — as long as you do your research.

What I think EVERYBODY should be doing when it comes to their investments is simple: low-cost, diversified index funds.

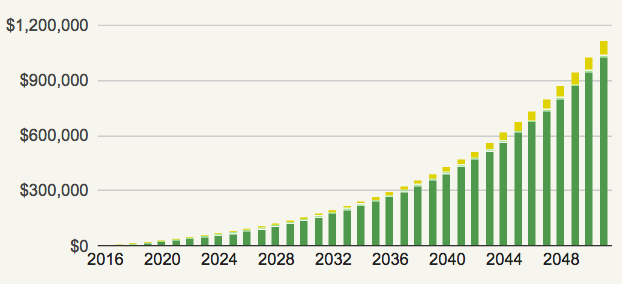

Let’s look at a real-world example.

Say you’re 25 years old and you decide to invest $500/month in a low-cost, diversified index fund. If you do that until you’re 60, how much money do you think you’d have?

Take a look:

[insert graph from original article]

$1,116,612.89.

That’s right. You’d be a millionaire after only investing a few thousand dollars per year.

Smart investments are about consistency more than chasing hot stocks or anything else:

The two essential ways to invest your money are straightforward:

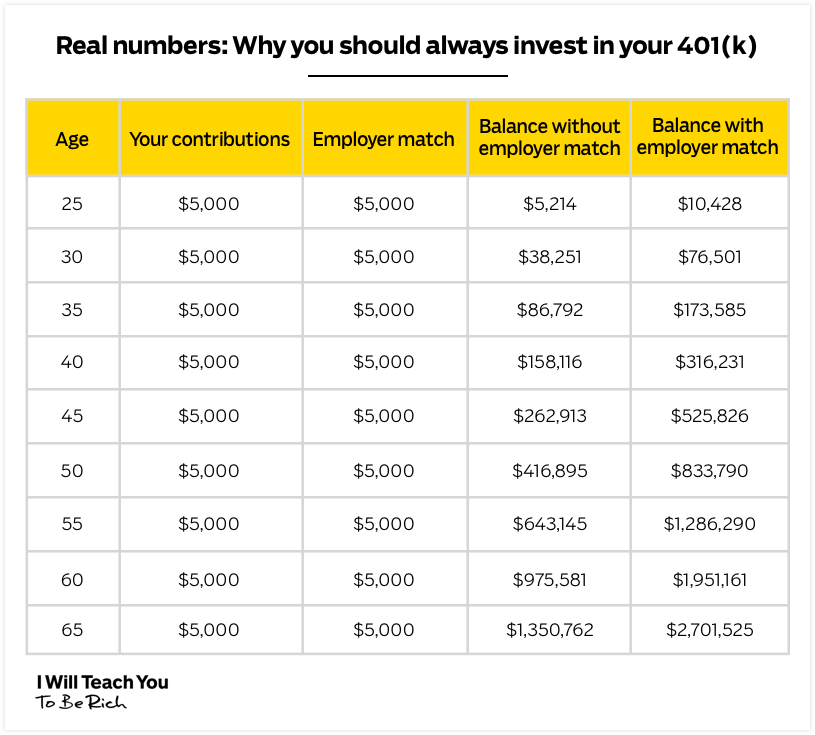

- 401k: Take advantage of your employer’s 401k plan by putting at least enough money to collect the employer match into it. This basically means that for every dollar you contribute, your company will match that (pre-tax!). This ensures you’re taking full advantage of what is essentially free money from your employer. That match is POWERFUL and can double your money over the course of your working life:

- Roth IRA: Like your 401k, you’re going to want to max it out as much as possible. The amount you are allowed to contribute goes up occasionally. Currently, you can contribute up to $6,000 each year.

Note: If $500/month sounds like a lot, read all the ways you can free up that money with just a few phone calls.

If you are just starting out, it’s so awesome that you’re here.

For financial security, it’s more important than anything else to start early. And don’t worry if you think you’re a little late to the game. After all, the best time to plant a tree was 20 years ago…the second-best time is NOW.

Man, I’m starting to sound like a fortune cookie.

Get started on your personal finance journey

If you’re looking into investment, congratulations! You’re making an important step in securing your financial future. Investment isn’t the only thing to think about though. Nor are stocks and bonds.

For a full-picture approach to personal finance, be sure to check out The Ultimate Guide to Personal Finance.

In it, you’ll learn not only how to understand stocks and bonds, but also how to:

- Master your 401k: Take advantage of free money offered to you by your company…and get rich while doing it.

- Manage Roth IRAs: Start saving for retirement in a worthwhile long-term investment account.

- Automate your expenses: Take advantage of the wonderful magic of automation and make investing pain-free.