What is a Good Debt To Asset Ratio? (Calculator + Ratios to Avoid)

A note on debt to equity ratio

Sometimes, lenders will look at a business’s debt to equity ratio instead. Chances are this doesn’t apply to 99.999% of you. But so you know, debt to equity looks at a company’s debt compared to shareholder equity (the value of the shares) and is calculated the same way as debt to asset ratio:

Debt to equity ratio

And then:

Like debt to asset ratio, your debt to equity ratio will vary from business to business.

However, general consensus for most industries is that it should be no higher than 2 (or 200%).

“But Ramit, I don’t have a big company or business. Does any of this matter to me?”

Yes! Because there’s a formula that creditors and lenders use to assess the risk of individuals like you.

Debt to income ratio calculation for individuals

If you plan on ever getting a mortgage for a house, you need to make sure your debt to income ratio is in check.

This number compares your gross monthly income to your monthly debt. Banks and other lenders look at this number to determine how much of a risk you are to lend to. The more of a risk you are, the less of a chance they’ll lend to you at all.

Much like your debt to asset ratio, calculating it is simple:

And then:

Let’s run an example scenario:

Say you owe about $1,000 in debt month-to-month and make $75,000 a year ($6,250/month). We’d then take 1,000 divided by 6,250 in order to get our debt to income ratio, like so:

Multiply .16 by 100 and you have 16% for your debt to income ratio….but what does that number mean?

What is a good debt to income ratio?

The lower the number is, the better. According to Wells Fargo, the ideal debt to income ratio is 35% and below. That said, most lenders will provide you a loan up to 43-45%.

So if your debt to income ratio amounted to 16% like in the example above, you’d be in good shape for a home loan.

If your debt to income ratio is a little higher and you want to lower it, though, I’d like to help you out.

After all, being in debt is the #1 barrier to living a Rich Life, and not only is it a financial burden, but it can also be a HUGE psychological burden as well.

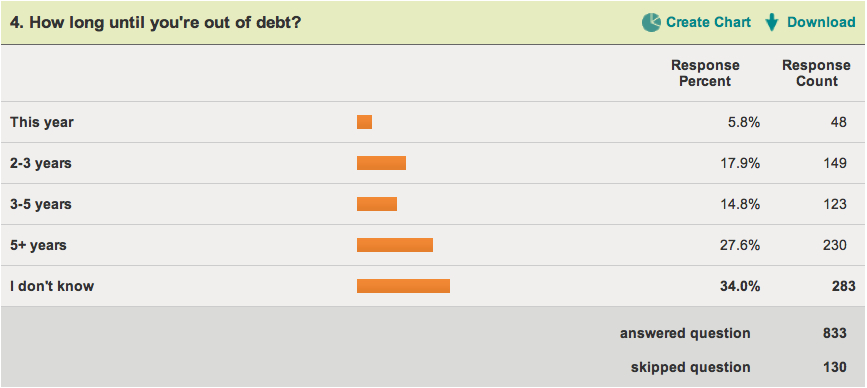

For example, a while back I ran a survey of my readers who were in debt, asking them a seemingly simple question: How long until you’re out of debt?

Take a look at the results:

34% (the majority) of respondents DIDN’T KNOW how long it would take until they were out of debt.

Debt is just as much of an emotional issue as a financial one. That’s why throwing a personal finance book at someone in debt or showing them a debt calculator produces little to no change.

If someone’s too afraid to even open the envelopes that will tell them how much they owe, “information” is not what they need. Instead, that person has to be willing to take action THEMSELVES before anything will change.

If you’re reading this now, and you’re ready to take action against your debt, I want to help you.

In fact, you can start getting out of debt TODAY through a 5-step system I’ve developed.

Just check out my popular article on how to get out of debt here.