Best Online Savings Accounts 2024 (NYT Bestseller’s Picks)

In today’s digital age, online savings accounts have gained significant popularity as a secure and convenient way to save money.

Whether you’re saving for a specific goal, building an emergency fund, or simply looking for a higher interest rate on your savings, online savings accounts offer a range of benefits.

Here are my picks for the best online savings accounts in 2024. (Please note: I have no affiliations with any of these companies.)

Table of Contents

If you want to skip all of that and open an account right now, these high-interest online savings accounts are my top-rated:

- Discover Online Savings Account

- Ally savings account

- Marcus by Goldman Sachs

- American Express savings account

- Barclays savings account

- Synchrony savings account

I believe you’ll be happy with any of them, but my personal favorite is Ally.

The Best Online Savings Accounts Of 2024

We’re going to do a deep dive into what to look for, which accounts are best, how to get the highest APY, and tricks for optimizing your savings accounts.

Online Savings Account Reviews

Here’s the lowdown on the most popular online savings accounts.

Axos Savings Account

- FDIC insured: Yes

- Minimum balance: None

- Maintenance fees: None

- APY: Up to 0.61%

The APY is much lower than other high-yield savings accounts—it’s average at best. There’s no reason to open an Axos account unless you’ve already maxed out the FDIC limits on every other high-yield savings account and have to get a lower APY to horde all your cash.

I recommend picking one of the other accounts from this list.

Discover Online Savings Account

Discover Online Savings Account

- FDIC insured: Yes

- Minimum balance: None

- Maintenance fees: None

- APY: 3.60%

Discover’s APY is pretty strong. Not quite the top, but it’s close.

And if you happen to have a Discover card or checking account, keeping your accounts in one place makes everything a lot simpler.

If you have another Discover account, definitely get a Discover savings account.

HSBC

HSBC has a few different savings accounts.

- FDIC insured: Yes

- Minimum balance: $100,000 across your deposit accounts and investment balances. If you go below this balance, there’s a $50 monthly fee.

- Maintenance fees: None

- APY: 0.15%

The HSBC Premier accounts are for clients who have large deposits at HSBC. Unfortunately, the APY is awful. An APY that low with a minimum balance of $100,000 is kind of insulting.

This is a good example of a classic big bank savings account. A bunch of constraints with a terrible APY. Skip these accounts entirely.

- FDIC insured: Yes

- Minimum balance: $1

- Maintenance fees: None

- APY: 0.01%

HSBC does have a high-yield savings account with a competitive APY. Normally, I’d recommend this account as a main contender.

But HSBC is just a terrible bank. Every interaction with them is more difficult than it has to be. The only reason I’d ever consider opening an HSBC account is if I needed a giant, international bank for some reason.

Ally Savings Account

- FDIC insured: Yes

- Minimum balance: None

- Maintenance fees: None

- APY: 3.75%

We’re huge fans of Ally. They’ve become one of the leading high-yield savings accounts.

Yes, Ally doesn’t technically have the highest APY, but it’s darn close. And they update their APY often. So if interest rates continue to rise, you’ll get a higher APY without having to do anything.

Their account UI is pretty slick too, and it’s always improving.

I have an Ally account myself.

Feel free to stop reading here and open an Ally account right now. You won’t regret it.

Capital One 360 Savings

- FDIC insured: Yes

- Minimum balance: None

- Maintenance fees: None

- APY: 3.4%

Capital One used to have an APY that lagged the rest of the market, making it a substandard choice. Now it has an APY that’s just as good as most banks. It’s one of the top contenders.

Especially if you have Capital One credit cards, it’s nice to keep everything at one bank.

Marcus by Goldman Sachs

- FDIC insured: Yes

- Minimum balance: None. However, , it does have a maximum limit of $1 million per account, not to exceed $3 million per account owner.

- Maintenance fees: None

- APY: 3.75%

Goldman Sachs jumped into the high-yield savings account space with one of the highest APYs.

They do limit deposits to a total of $1,000,000, but that’s not a major concern. You’ll want to split up your cash balances across multiple banks to get it all FDIC-insured anyway.

If you’re looking for your first high-yield savings account, this is a fantastic option.

American Express Savings Account

American Express Savings Account

- FDIC insured: Yes

- Minimum balance: None

- Maintenance fees: None

- APY: 3.75%

American Express was one of the first to introduce a high-yield savings account, and it’s been around for a while now.

You can set up and start using your American Express High Yield Savings in minutes. You can also have multiple linked accounts and move money between them.

Barclays Savings Account

- FDIC insured: Yes

- Minimum balance: None

- Maintenance fees: None

- APY: 3.60%

Another great option. Great APY, no maintenance fees, or minimum balances—you can’t go wrong with a Barclays online savings account.

Synchrony High Yield Savings

- FDIC insured: Yes

- Minimum balance: None

- Maintenance fees: None

- APY: 4.0%

Synchrony is also a great option. The APY is one of the highest and has no minimums or maintenance fees. Plus, you can earn a variety of perks, such as ATM fee reimbursements.

Vio Bank

- FDIC Insured: Yes

- Minimum Deposit: $100

- Maintenance Fees: None

- APY: 1.10%

Because Vio Bank has no ATMs, cash cannot be deposited into a savings account. To transfer money into a savings account, link it with your current (external) bank checking account. Direct deposits can be made into your savings account.

Bread Savings High-Yield Savings Account (formerly Comenity Direct)

Bread Savings High-Yield Savings Account

- FDIC Insured: Yes

- Minimum Deposit: $100

Maintenance Fees: None - APY: 4.50%.

With this account, there is no monthly maintenance fee. You also won’t get charged for ACH transfers, online statements, or incoming wire transfers. However, you’ll pay $25 per outgoing wire transfer, $15 per official check request, and $5 each time you request a paper statement.

To take cash out, you must transfer money to a linked account. Bread Savings doesn’t offer ATM cards, debit cards, or checks with this account.

Citizens Access

- FDIC Insured: Yes

- Minimum Deposit: $1

- Maintenance Fees: None

- APY: 4.25%

Citizen’s Access APY is very competitive, and they rank high for their CDs as well. Citizen’s Access doesn’t have a mobile app, and they don’t offer any checking accounts, so you’ll have to split your funds between two financial institutions.

…but you don’t have to take the same path as everyone else. How would it look if you designed a Rich Life on your own terms? Take our quiz and find out:

What Matters When Choosing An Online Savings Account

When it comes to choosing an online savings account, several key factors should be taken into consideration. Choosing the right account can make a significant difference in the growth and accessibility of your savings.

Here’s how we evaluate these accounts.

User Experience And Company Reputation

Good online and mobile apps make a huge difference these days, but it doesn’t matter as much when you’re looking for a high-interest online savings account.

It needs to be good enough, but not great.

Why?

Because we rarely log into savings accounts. They usually have limits for withdrawals up to 6 times per month. By definition, they’re not meant to be used regularly.

Having quick and easy access to your funds is less important than working with a company that has a reliable reputation.

While most customers can access their high-interest-rate accounts quickly in an emergency, not all financial institutions are created equal. We skipped companies that scored less than 65 percent of the Harris Poll Corporate Reputation Rankings, like Wells Fargo, and Bank of America. We also factored in major scandals over the last five years.

Fees

For online savings accounts, it’s essential that you get an account without any maintenance fees. Monthly maintenance fees used to be common. Thankfully, most accounts have done away with them.

On any good savings account, you’ll rarely run into fees during normal usage. But even on the best accounts, it is possible to trigger fees for certain events:

- Returned deposit items

- Overdraft items paid or returns

- Excessive transaction fee (like going over 6 withdrawals per month)

- Expedited delivery

- Outgoing domestic wires

- Account research fees

We’ve made sure not to include any banks on our list that have maintenance fees. But you should be aware of some of these other fee items that do exist on every account.

Avoiding bank fees and charges is a key part of getting a handle on your money.

Convenience

What we consider to be “convenient” with savings accounts falls into two buckets depending on where you are in your own personal finance journey.

When you’re building savings for the first time, it’s essential to get an account with no minimum balance requirement. A $5 required balance or something like that is fine; you just don’t want to worry about a higher one.

Don’t put up with any account that requires a sizable minimum balance. There are so many options that don’t have any balance requirements at all. This is the last thing you should be worried about in the early days, especially if an emergency comes up and you need to withdraw cash.

Later on, what you consider to be convenient typically changes.

Once you’ve built enough of a cash buffer for yourself, you’ll care a lot less about minimum balances. Instead, your accounts, cards, and banks will all have gotten complicated enough that simplicity will matter a lot more than it used to. At this stage, some folks will opt for a lower APY to consolidate their accounts and make everything more manageable.

Is this the optimum strategy to get every ounce of growth from your cash? No, it isn’t. But the extra peace of mind can be well worth the cost. If this sounds appealing to you, check to see if the savings account at your main bank has a good enough APY without any maintenance fees. If it does, it could be your best option.

FDIC-Insured

Don’t ever consider an online savings account that’s not FDIC-insured. This means that the account is guaranteed by the federal government up to $250,000 per depositor. If something horrible happens to the bank, the federal government guarantees you’ll still get access to your balance, up to $250,000. This is per depositor, so the $250,000 includes the combined balance of all your savings accounts at the same bank.

Nearly every savings account is FDIC-insured, as it’s been a standard practice for a long time. But keep a close eye on this any time you’re considering an innovative or unique approach to storing your cash.

For example, some folks will store their cash in a money market account, which operates a lot like a savings account. Money market accounts are usually FDIC-insured. But money market funds, which you place cash into from a brokerage account, are not FDIC insured. A subtle yet critical difference during tenuous times.

Another example: Robinhood attempted to roll out a checking account that promised a 3% APY. That’s a checking account paying higher interest than any savings account that was available at the time, by almost 1%. Sounds amazing, right?

It came with several catches, one of which was that it wasn’t FDIC-insured. Without FDIC insurance, the higher APY is not worth the risk.

My stance is that every dollar of our savings should be covered by the FDIC, even if the balance is high enough that we have to split it up between multiple savings accounts.

All of the accounts that we reviewed are FDIC-insured. Just keep an eye out for this if you’re exploring an atypical approach to storing your cash.

APY Rates

APY rates—the annual percentage yield—are the main difference between savings accounts. The higher your APY rate, the more money you get automatically every month.

APY rates across saving accounts generally fall into 3 tiers.

Big bank savings account APYs

For the vast majority of big bank savings accounts, the APY is terrible. Big banks assume that you want a savings account along with your checking account, so they don’t do anything to entice you to the savings account itself. Even when plenty of online high-yield savings accounts are offering an APY of 2%, big banks might only offer a 0.15% APY. On a savings balance of $10,000, that’s a difference between making $200 a year versus $20 a year.

This doesn’t apply to ALL big banks, but most of them do fall into this category. So keep an eye out for these. Unless you really want to maximize convenience by consolidating accounts and taking a lower APY, it’s worth finding an account with a higher APY.

High-yield savings account APYs

High-yield savings accounts have become extremely popular. These banks don’t have branches; they’re 100% online. Since they save a lot from not having physical locations, they pass the savings onto you with a higher APY.

Ally and American Express are two of the most popular banks in this category.

The APY also stays updated over time. Back during the financial crisis, the Federal Reserve dropped interest rates to 0%, and most high-yield savings accounts had APYs of 0.5-0.7%. As the Federal Reserve increased interest rates, these same accounts also increased their APY. Whenever interest rates increase, you’ll get those increases automatically from these accounts. No need to constantly switch between accounts and chase the best rate.

Cutting-edge APYs

At any given moment, there are a few banks that are pushing the APYs higher than anyone else. They’re doing this as a promotional strategy to attract more customers. Some of these banks keep pace with changing interest rates, and some of them don’t.

While we don’t consider it worth the effort to chase an extra 0.1% on our APY, these banks are an option if you’re looking to maximize the APY on your savings.

Budgeting is unsustainable. Start “Conscious Spending” instead.

As seen on the IWT podcast, my Conscious Spending Plan helps you buy the things you love, guilt-free.

The 4-Step Process To Choosing The Best Online Savings Account

Check the banks that you currently have accounts with and see if they have competitive savings accounts. If the APY is comparable to the accounts we listed above, stick with your current bank.

Otherwise, pick an account from this list:

- Try to pick an account from a bank that you foresee doing other business with. For example, Ally has car loans, and Discover has their credit cards.

4. If you’re still not sure, go with Ally.

What About Sub-Savings Accounts?

One of our favorite savings account tricks is to open “sub-saving accounts”. This allows us to easily budget for bigger purchases by saving a little bit each month. We can also track everything by separating all the accounts.

For example, I have these categories in my own savings account:

- Emergency fund

- House down payment

- Mini-retirement

- Christmas gifts

- Annual vacation

Each month, money goes into each of these separate accounts with the automatic transfers that I set up. And I can easily see how much I’ve saved towards my goals. If you’re like me and you also plan for an annual vacation, have a look at this video, which will help you even more in how to plan and save for it.

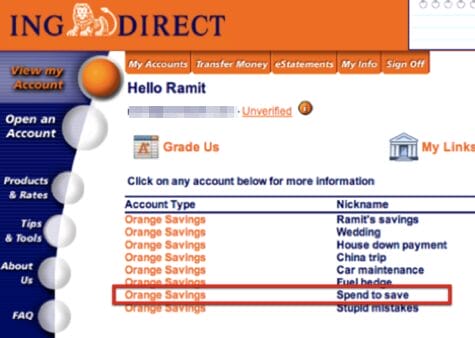

My savings accounts used to look like this back before ING Direct was bought by Capital One:

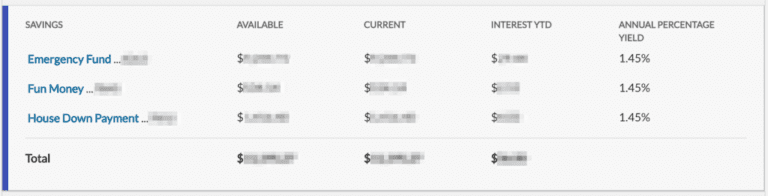

Here’s a more current example in Ally:

Some savings accounts will call these “sub-accounts,” and everything will be part of the same savings account. This is a rare feature to find, though.

For everyone else, simply open up multiple savings accounts under the same bank login. You can easily have 5-10 accounts at the same bank. Then treat each account for whatever saving category you like.

This means you can get “sub-accounts” at any bank, even if they don’t have a “sub-account” feature.

Don’t Chase Yields

Look, there’s always a bank that has a slightly higher APY. Banks use it as a promotion strategy to get more accounts, so it’s always changing.

Regularly researching new APY rates, looking for that extra 0.05% APY, opening accounts, and transferring money all over the place wastes more time than it’s worth.

Don’t be a rate-chaser.

Remember IWT’s philosophy of big wins: Focus on the major wins that really move the needle and forget about the small stuff. Chasing higher APYs on savings accounts definitely falls into the “small stuff” category.

Pick a savings account that has a competitive APY from a bank that you trust for the long term. Then stick to that decision and work on improving other areas of your life.

Money Market Accounts vs. Savings Accounts

The difference between money market accounts and savings accounts can be pretty confusing.

That’s because there’s no practical difference.

Here are the similarities:

- The APY tends to be the same between both types of accounts

- You can withdraw up to 6 times per month

- Some have ATM cards, some don’t

- Some have minimums, and some don’t

- Both are FDIC-insured

Basically, they’re the same account. If your bank offers a money market account with no maintenance fees, no minimum, and a competitive APY, feel free to use it.

Now for the confusing part: money market funds are completely different. They’re part of brokerage accounts and allow you to place cash while you wait to invest it. Since money market funds are not FDIC-insured, it’s not a good habit to store lots of cash in them.

When To Get Savings Accounts From Multiple Banks

If you ask high-net-worth folks which savings account they have, sometimes they’ll list off half a dozen different banks.

At first, this makes no sense. Why all the extra complexity and different accounts?

There’s one reason: FDIC insurance limits.

Most people are limited to $250,000 worth of insurance at any given bank. Joint accounts and accounts across different categories (like retirement accounts) can increase this limit, but that only goes so far. If you have a substantial amount of cash, the only way to keep it insured is to open up savings accounts across several banks.

That’s why folks will start opening up savings accounts across multiple banks.

If you have multiple savings accounts to manage, Max will automatically move balances around your accounts to optimize for the highest APY while keeping all your cash insured. They do charge a 0.08% annual fee for the service.

Frequently Asked Questions About Online Savings Accounts

Are online savings accounts safe?

Online savings accounts offered by reputable financial institutions are generally safe. Look for banks that are FDIC-insured, which means your deposits are protected up to the maximum limit allowed by law.

What are the pros and cons of high-yield savings accounts?

High-yield savings accounts offer several advantages, including competitive interest rates that help your savings grow faster, safety through FDIC or NCUA insurance, easy accessibility to funds, and low or no fees. However, there are a few drawbacks to consider. Interest rates can fluctuate; limiting the number of transactions or withdrawals per month is common, and the returns may be lower compared to long-term investments. Additionally, some high-yield savings accounts are offered exclusively online.

How many savings accounts can you have?

There’s no limit to the number of savings accounts you can have. It’s all about what makes sense for your financial goals and organization strategy. Some people open multiple accounts to earmark funds for specific purposes like emergency savings, vacations, or big purchases. Just keep an eye on any minimum balance requirements or fees to ensure you’re not spreading your funds too thin. Managing multiple accounts wisely can be a powerful tool in achieving your financial objectives.

How much money should I keep in my savings account?

A savings account is where you stash cash not meant for daily expenses. Ideal for your emergency fund or saving towards goals like a holiday or home down payment. The right amount in your savings depends on your individual goals. Unlike checking accounts, savings accounts earn interest, rewarding you for storing your money there. The better the interest rate, the quicker your savings increase.

This makes choosing the best savings accounts a critical step for anyone aiming to maximize their savings growth efficiently.

What is the highest interest savings account?

The highest interest rates for savings accounts often come from online banks, which can offer more competitive rates than traditional brick-and-mortar banks due to lower overhead costs. High-yield savings accounts might offer rates significantly above the national average, but these rates can fluctuate with the market. To find the highest interest rates, it’s essential to shop around and check the latest offers, as they can change frequently based on economic conditions.

If you liked this post, you’d LOVE my New York Times Bestselling book

You can read the first chapter for free – just tell me where to send it:

Written by Ramit Sethi

Host of Netflix’s “How To Get Rich” NYT Bestselling Author, & Host of the I Will Teach You To Be Rich Podcast. I’ll show you how to take control of your money with my proven strategies so you can live your RICH LIFE.